PCCA Cotton Market Weekly

March 14, 2025

Cotton prices recovered slightly this week, although fundamentals remain bearish. Stock markets struggled with ongoing trade tensions and economic concerns. Will cotton continue to trade within a range, or will outside factors push it lower again? Get QuickTake’s read on the week’s events in five minutes.

Cotton prices regained some of last week’s losses but faced continued headwinds from outside markets.

- The May contract settled at 66.53 cents per pound, up 132 points for the week.

- Cotton futures closed at a two-week high, likely driven by speculative short covering after reports of a record net short position. The futures market didn’t react to the few changes in Tuesday’s World Agricultural Supply and Demand Estimates (WASDE) Report. Despite a strong Export Sales Report, outside market forces pressured cotton. The AWP moved above loan Friday, which caused heavy cotton loan redemptions by the Thursday deadline. That cotton was likely hedged, producing downward pressure on the market at the week’s end.

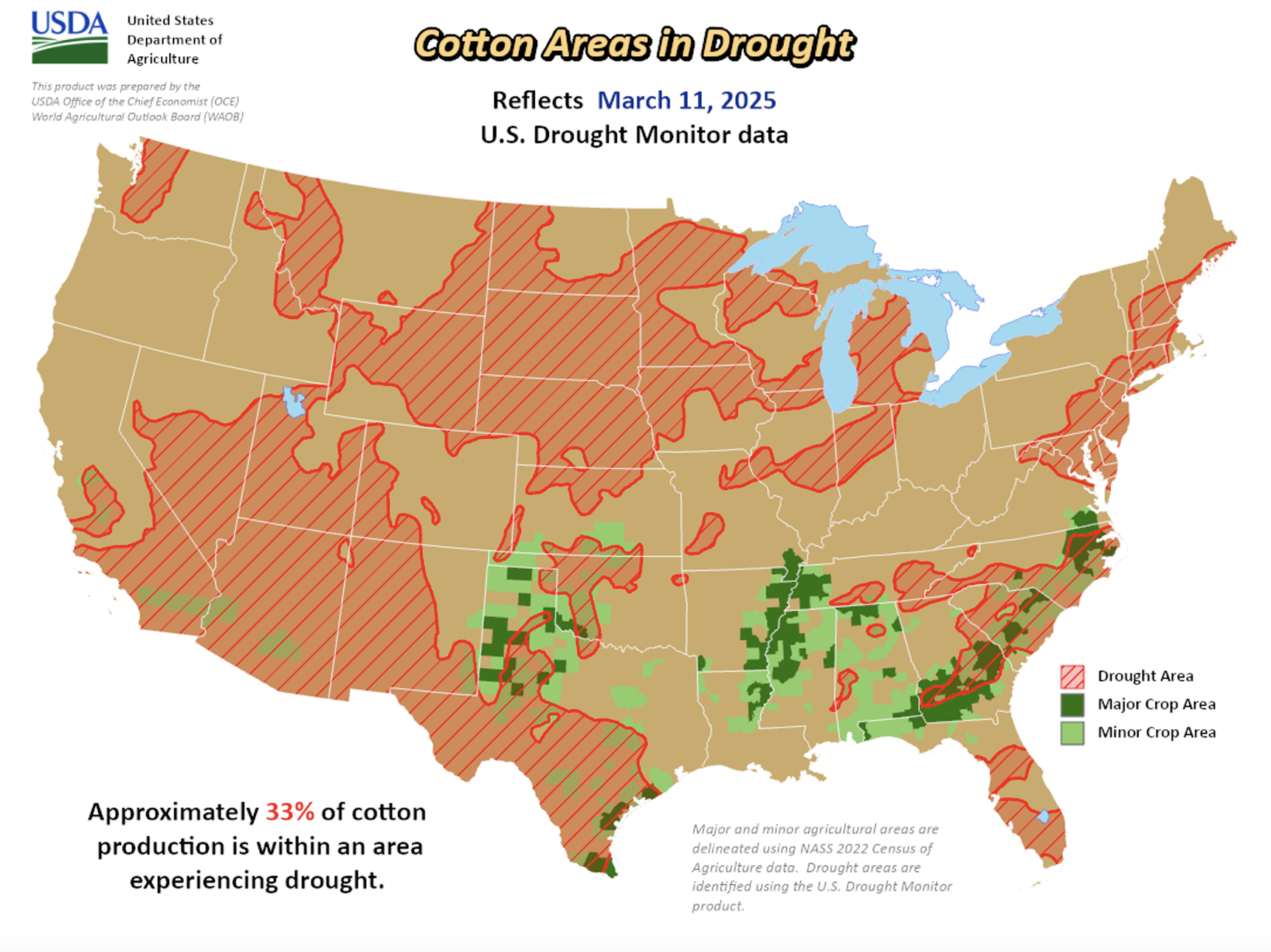

- Planting has begun in the southernmost part of Texas. Soil moisture is low, and recent temperatures have not alleviated the dryness the region has experienced in recent months. Rain and more seasonable temperatures are desperately needed in the near term to support planting.

- Trading volumes moderated after last week’s record volume. Open interest rose by 8,300 contracts, bringing the total to 273,897. Certificated stocks were last reported at 14,488 bales, an increase of 55 bales.

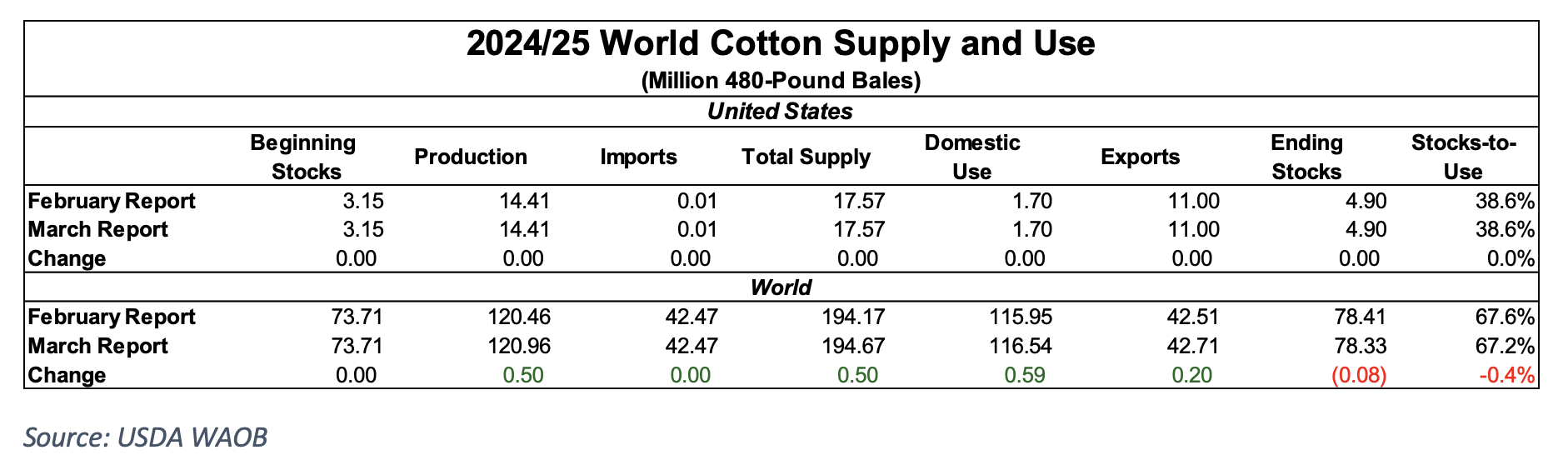

USDA’s March release of updated supply and demand numbers was underwhelming.

- The U.S. balance sheet remained unchanged, with production holding steady at 14.41 million bales and exports at 11 million bales. Consumption remained at 1.7 million bales, while ending stocks stayed at 4.9 million bales, resulting in a stocks-to-use ratio of 38.6%. This kept the U.S. balance sheet looser than usual.

- The global balance sheet saw some notable changes, though none significant enough to disrupt the market. World production rose by 500,000 bales to 120.96 million, driven mainly by a 750,000-bale increase in China’s output to 31.75 million. Chinese imports dropped 500,000 bales to 6.8 million, with Pakistan and Bangladesh absorbing the shift, increasing their imports to 5.5 million and 8.2 million bales, respectively. Brazilian exports rose by 200,000 bales to 13 million.

- Meanwhile, world ending stocks fell by 80,000 bales to 78.33 million, while consumption climbed 590,000 bales to 116.54 million, lowering the stocks-to-use ratio to 67.2%.

The downward slide in equities continued amid recession fears, trade tensions, and talks of a government shutdown.

- The dizzying implementation and rollback of tariffs continued. On Wednesday, the Trump administration imposed 25% tariffs on all U.S. steel and aluminum imports. Europe and Canada quickly retaliated with duties on American goods.

- As if the volatility surrounding tariffs were not enough, government shutdown fears took center stage this week. The Continuing Resolution (CR) passed in December is set to expire on March 14. The House approved a new CR to fund the government through September. Many believed that was the biggest hurdle, but once the bill reached the Senate, tensions escalated, and it became unclear whether there were enough votes to meet the 60-vote threshold needed for it to pass. As of this writing, however, the Senate had signaled its support, saying that a vote to approve the funding measure would move forward.

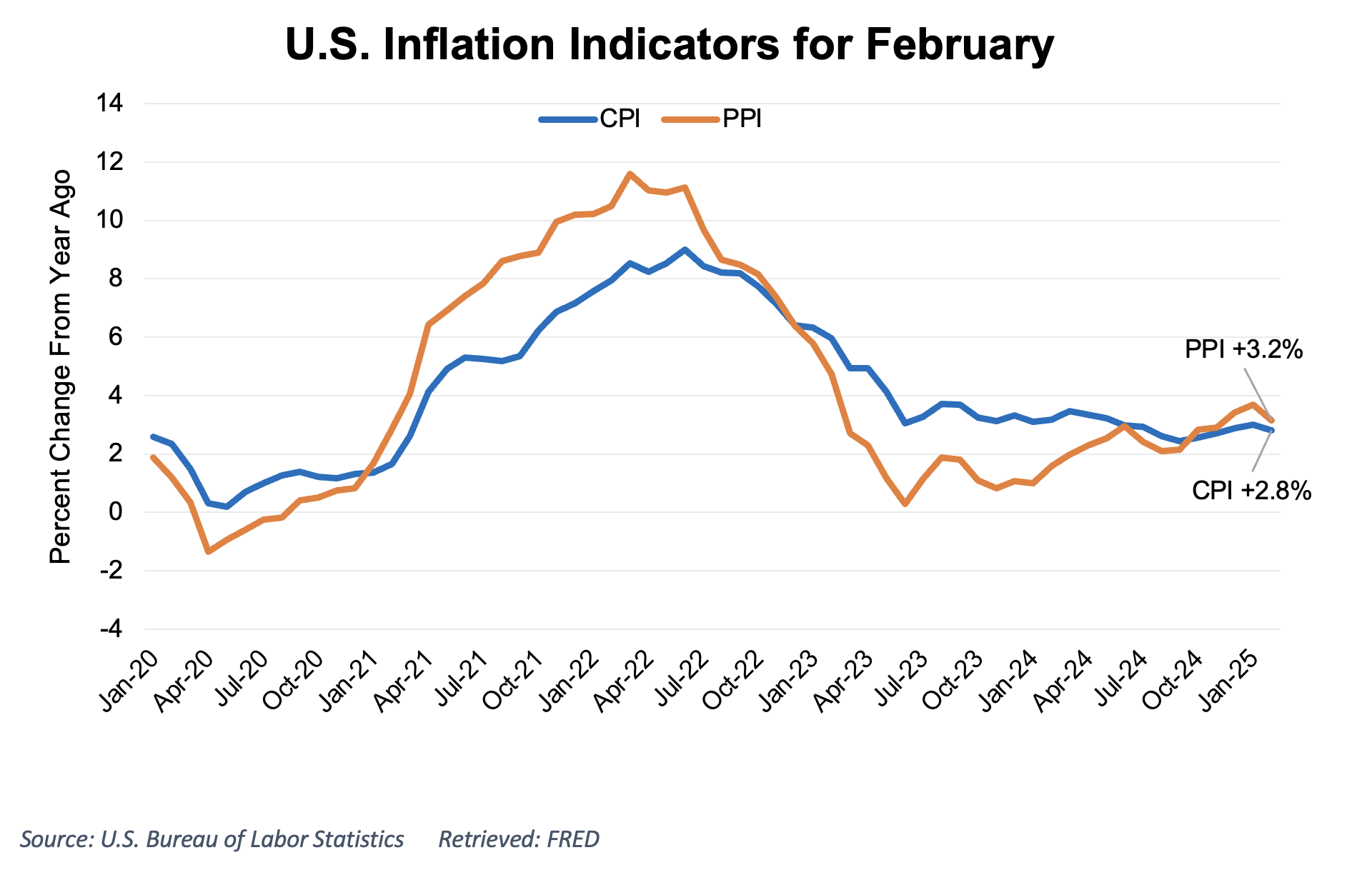

- The U.S. Consumer Price Index (CPI) and Producer Price Index (PPI) provided an updated look at inflation for February. CPI increased 0.2% month-over-month and 2.8% year-over-year, slightly below expectations. PPI was steady for the month and increased 3.2% on the year, both below expectations.

- The U.S. dollar index was down most of the week but rose due to escalating trade war concerns. A weaker dollar is bullish for U.S. commodities, as it makes dollar-denominated goods more affordable for importing countries.

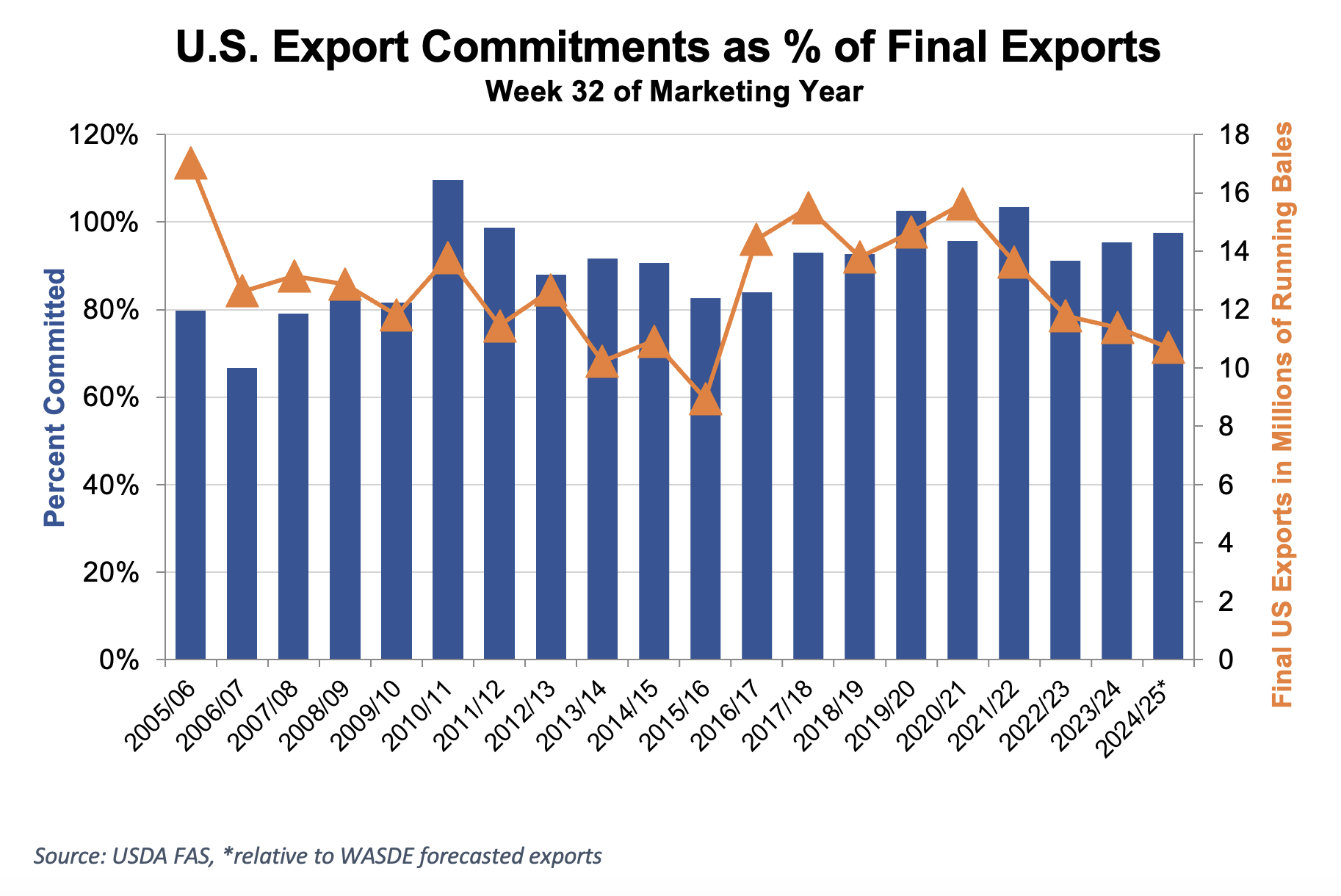

Thursday’s Export Sales Report showed another week of strong sales and a marketing-year high in shipments.

- For the 2024/25 marketing year, U.S. merchants sold 241,500 Upland bales and shipped a marketing-year high of 334,000. Both sales and shipments were strong, exceeding the pace needed to meet the USDA’s current export estimate of 11 million bales.

- An interesting development in recent Export Sales Reports has been the increase in new crop sales. A total of 110,200 bales were booked for the week, which is well above the typical amount sold for this time of year. While it’s too early to call it a trend, we will continue to monitor new crop demand to gauge global interest in U.S. cotton for the next marketing year.

- Pima sales and shipments slowed compared to previous weeks, with merchants selling 4,600 bales and exporting 6,900 bales.

The Week Ahead

- Tariff threats, impositions, and retaliation will be monitored again next week. Additionally, updated U.S. retail sales data will be released on Monday.

- The Federal Open Market Committee (FOMC) meeting will begin on Tuesday, March 18, with an interest rate decision expected on Wednesday, March 19. Most expect rates to remain steady at 4.25% to 4.5%.

Announcements

- Enrollment for the U.S. Cotton Trust Protocol is now open through April 30, 2025. Currently enrolled growers will need to renew their membership to continue their involvement in the program.

- New Grower Enrollment for Better Cotton will be open March 3-May 30.

- For assistance or questions about enrolling in these programs, contact PCCA at 806-763-8011.

The Seam

As of Thursday afternoon, grower offers totaled 139,829 bales. There were 19,307 bales that traded on the G2B platform with an average price of 61.99 cents per lb. The average loan was 52.12, resulting in a premium of 9.87 cents per lb. over the loan.