PCCA Cotton Market Weekly

December 15, 2025

The Week Ahead

- Looking ahead, agricultural markets remain seasonally supported but vulnerable to short-term volatility. The U.S. dollar softness is supportive of exportable commodities like cotton, but a stream of belated economic data may drive sharp price swings. As markets enter the strongest seasonal window of the year, pullbacks may continue to attract buying across the ag complex. This week is shaping up to be busy, with unemployment reports, delayed retail sales, and updated inflation data alongside the usual cotton reports.

Market Recap

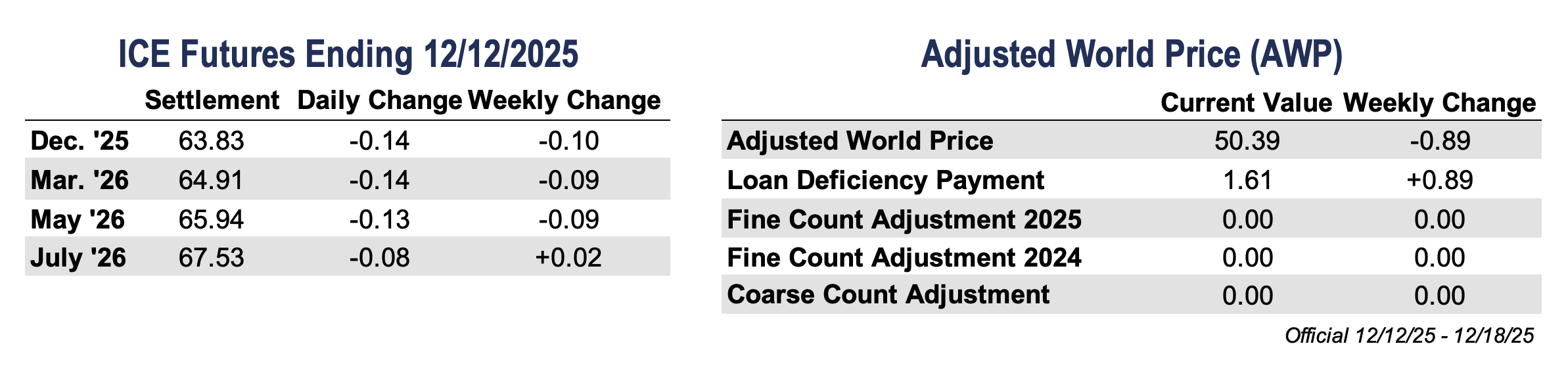

- Cotton futures traded in a narrow, mostly sideways pattern last week, with March futures posting a small net loss. Daily ranges remained tight, and March settled Friday a marginal 10 points lower at 63.83 cents per pound as the market continued to search for direction.

- Cotton-specific news remained limited, with much of the focus on shutdown-delayed reports still working their way through the system. Export Sales were mixed, and the December supply and demand report was largely taken in stride. Futures took little direction from outside markets despite a 25-basis-point Fed rate cut that supported equities, as cotton remained weighed down by steady selling. The tone stayed subdued throughout the week, with technicals still pointing to limited upside momentum. In a switch, speculators were net buyers for five consecutive weeks through November 18 based on the latest available data, which was delayed by the government shutdown, even as the market posted a contract low.

- Holiday trading has kept volume moderate; however, open interest increased by 5,564 contracts to 292,305. Additionally, 1,614 bales were decertified, bringing certificated stocks down to 13,971 bales.

Supply and Demand Overview

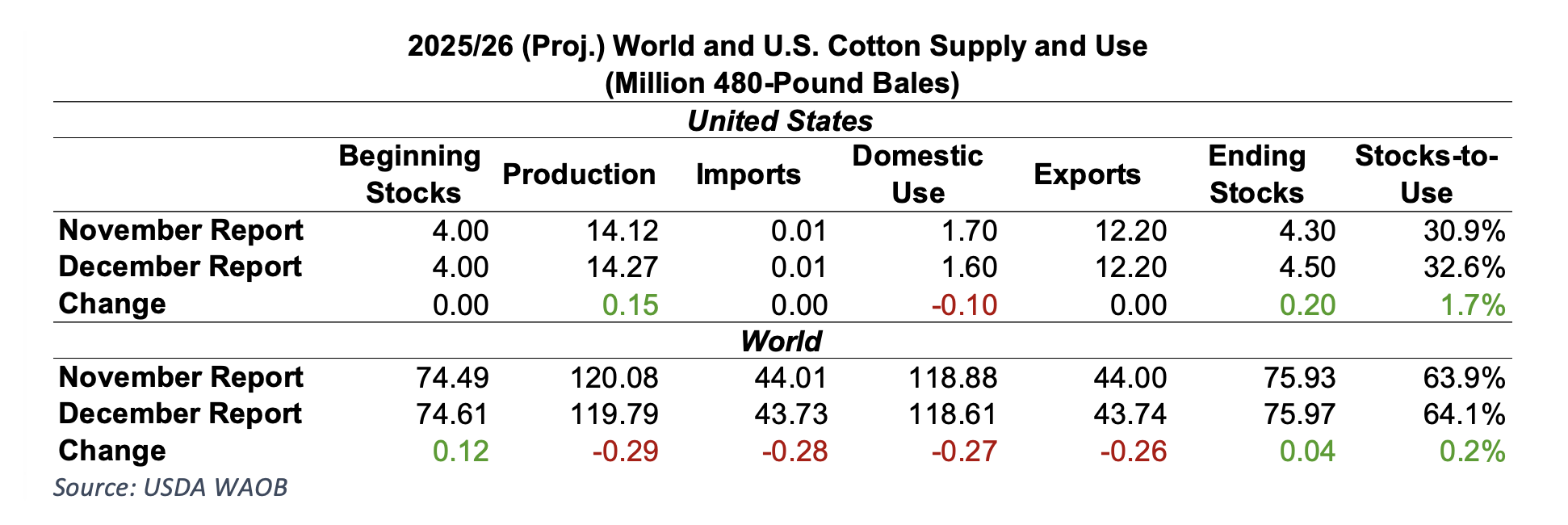

- The December World Agricultural Supply and Demand Estimates (WASDE) was greeted with a yawn. While most agreed with the overall balance sheet, analysts strongly disagreed with the regional production estimates. U.S. production was increased to 14.27 million bales, driven by gains in the Mid-South and Southeast, while the Southwest saw a net decline. Texas production was reduced by 300,000 bales to 5 million, Oklahoma fell 20,000 bales to 450,000, and Kansas remained unchanged at 150,000 bales. U.S. domestic consumption was also lowered by 100,000 bales to 1.6 million bales, while exports were left unchanged at 12.2 million bales, pushing ending stocks higher to 4.5 million bales and keeping them elevated.

- A familiar theme of global use estimates receding during the season seems to be developing again. Consumption slipped 270,000 bales to 118.61 million bales, while production declined 290,000 bales to 119.79 million. World ending stocks edged up to 75.97 million bales. Despite some debate around the state-by-state U.S. adjustments, changes to both the U.S. and world balance sheets were relatively modest, which is typical for the December report.

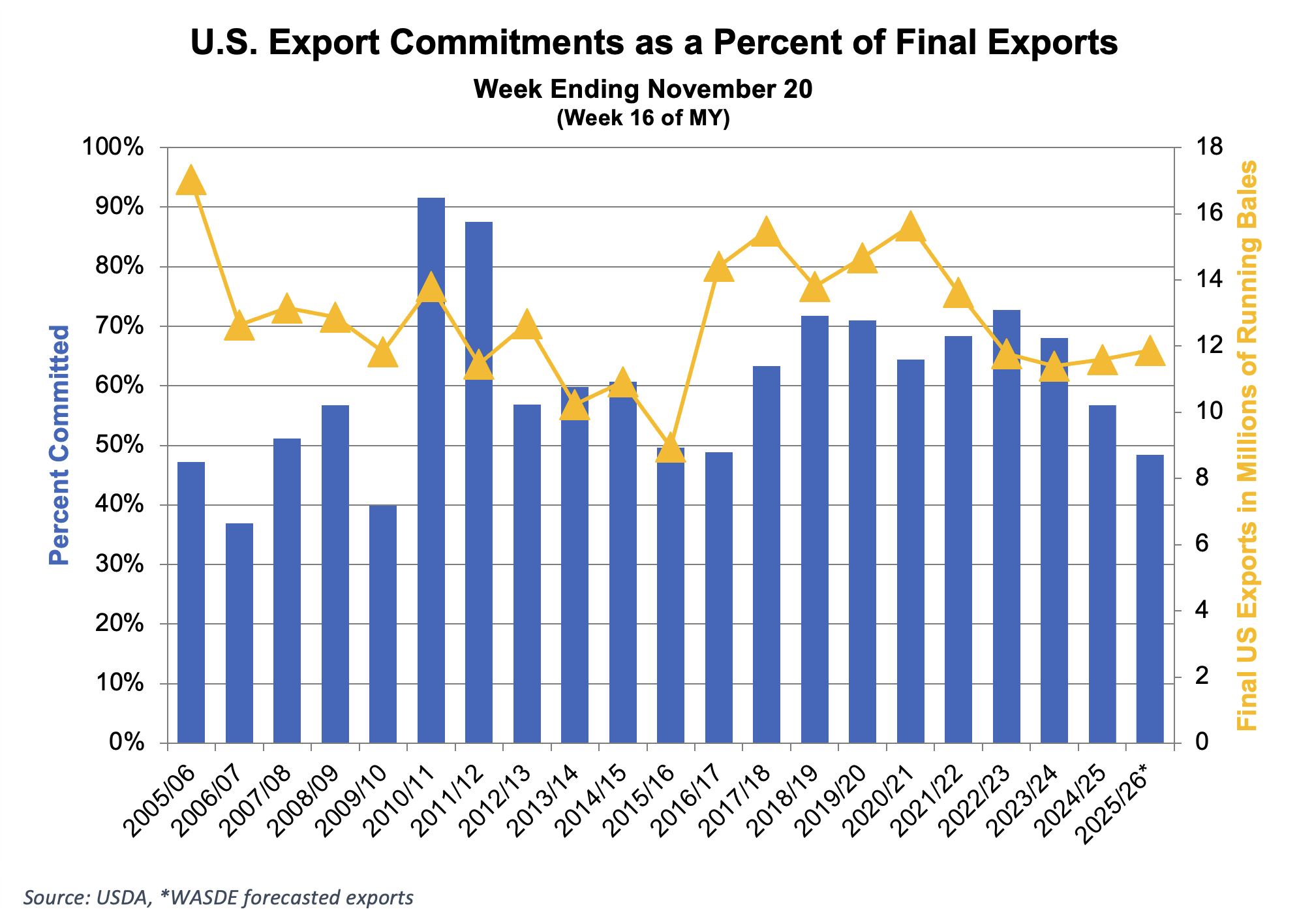

- For the week ending November 13, net Upland sales totaled 187,600 bales, with shipments at 113,200 bales, led by buying from Vietnam, Turkey, and Pakistan. Pima bookings reached 8,900 bales, with shipments totaling 7,800 bales.

- The following week, ending November 20, net Upland sales eased to 148,400 bales, while shipments increased to 120,800 bales. Vietnam, Turkey, and Pakistan once again led weekly buying. Pima net sales came in at 6,200 bales, with shipments at 6,700 bales. Even so, total commitments and shipments remain behind the pace needed to reach USDA’s export projection of 12.2 million bales. USDA is still working through data delays tied to the government shutdown but is expected to be fully caught up with the Export Sales Report on January 8.

Economic and Policy Outlook

Economic and Policy Outlook

- President Trump announced the Farmer Bridge Assistance Program during a White House roundtable with farmers, outlining a $12 billion economic aid package for the 2025 crop year, including $11 billion earmarked for row crops. The ECAP-styled program is designed to provide near-term financial support until expanded benefits under the One Big Beautiful Bill Act take effect in fall 2026. Commodity-specific per-acre payment rates are expected the week of December 22 and will be based on USDA cost-of-production estimates and projected marketing-year prices. Producers must have acreage on file with USDA FSA by December 19, with payments expected by February 28, 2026, subject to payment and income limits. The relief is good news but featured an unwelcome new payment limit of $155,000 vs $250,000 in many recent packages, such as ECAP.

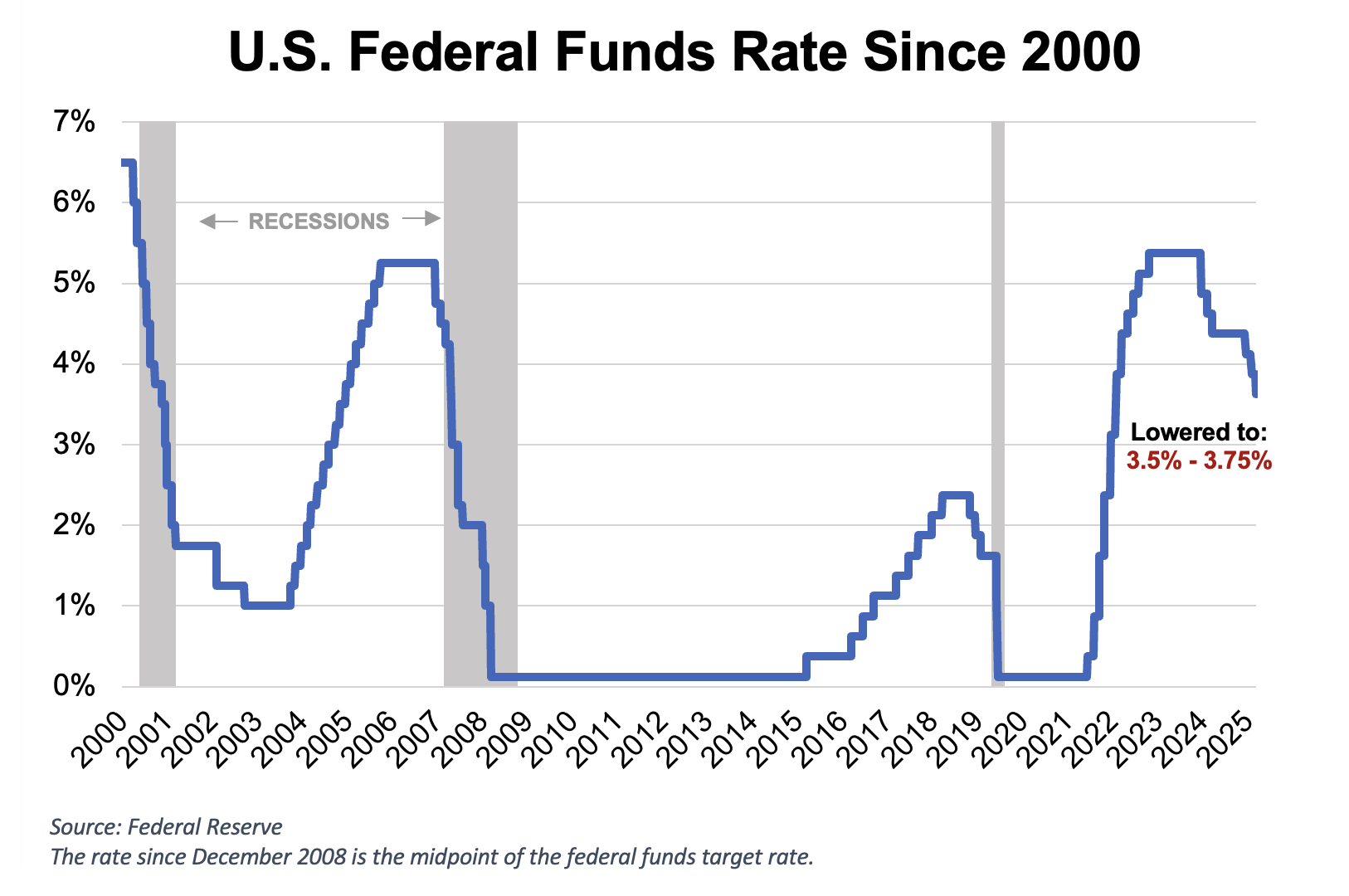

- The Fed delivered a third straight 25-basis-point rate cut last week, lowering the target range to 3.50–3.75% and striking a notably dovish tone. Chair Powell pointed to softening labor conditions and suggested recent payroll data may be overstated, while noting policy is now near neutral but still tilted toward easing. Markets responded quickly, with two-year yields posting their largest one-day drop in two months, the dollar sliding, and equities moving higher. Looking ahead, focus turns to this week’s delayed November payrolls and Thursday’s CPI, which could further shape expectations for additional rate cuts in 2026.

Weather and Crop Watch

Weather and Crop Watch

- Harvest made steady progress last week as warm, dry conditions across the Southwest allowed fieldwork to move along with few interruptions. A brief cold front passed through late in the week, but its impact was limited, and with much of the crop already off the stalk, attention continues to shift toward ginning activity. Looking ahead, the extended dry forecast and a return to warmer temperatures should provide a clean window to wrap up harvest and keep ginning operations moving efficiently.

- Classing continues across the Cotton Belt, and based on current USDA crop size estimates, roughly 70% of the Southwest crop has been classed. Quality in West Texas has fallen a little the past week, with the amount of tenderable cotton slipping due to a modest uptick in bark and slightly shorter staple in some areas. That said, grades, micronaire, uniformity, and strength have remained steady.

The Seam

- As of Friday afternoon, grower offers totaled 135,094 bales. The past week 35,085 bales traded on the G2B platform received an average price of 59.81 cents per pound. The average loan redemption rate (LRR) was 53.60, bringing the average premium over the LRR to 6.21 cents per pound.

- *Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).