PCCA Cotton Market Weekly

December 22, 2025

The Week Ahead

- Macro sentiment has stabilized after last week’s cooler inflation print, but signals remain mixed for ag, with a firmer Chinese yuan offset by a softer Brazilian real. On top of that, speculators continue to short the market. This week will be relatively quiet on the data front, with markets watching U.S. Gross Domestic Product (GDP) and consumer confidence. Typical holiday trading has set in, keeping markets quiet into year-end, with liquidity expected to remain thin. Price action in the cotton market will largely respond to broader macro moves in equities, energy, and the dollar. That said, we have entered the most seasonally supportive window of the year for cotton, with historical tendencies favoring strength into mid-February. With the Commitments of Traders (COT) data finally caught up this week and index rebalancing ahead in early January, the setup leaves room for stabilization and potential recovery as we head into 2026, and there’s a lot of room for recovery.

- Markets will be closed on Thursday, December 25. For cotton, this means an early close on Wednesday at 12:00 p.m. CST, followed by a late open on Friday at 6:30 a.m. CST with regular closing hours.

Market Recap

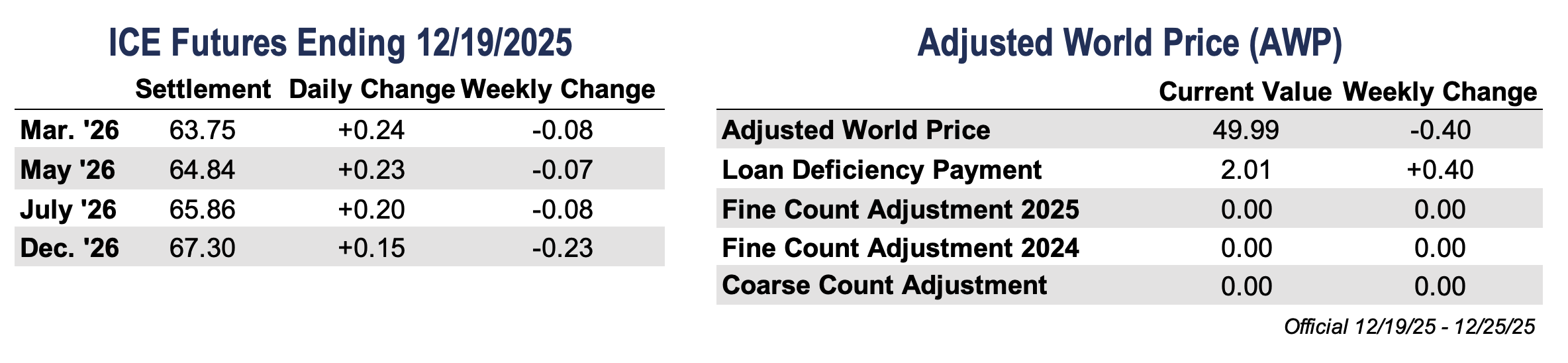

- Cotton futures recouped some early-week losses after hitting a contract low last Tuesday. The market posted three consecutive sessions of modest gains, though buying interest remained limited. March futures settled just 8 points lower on Friday at 63.75 cents per pound, as the market continues to search for direction.

- Unemployment data pressured prices and pushed the cotton market lower through key technical levels, though support was eventually found. In the days that followed, prices drifted higher, helped by cooler inflation data and firmer crude oil prices. With the technical outlook still weak, specs remaining net short, and supportive news limited, this backdrop suggests cotton prices will be choppy in the near term, particularly as funds continue to reduce exposure.

- Additionally, quality in West Texas deteriorated slightly over the past week, due to increased extraneous matter showing up in classing samples. Attention remains on ginning and classing activity as both progress, while concerns are also building around moisture for next season. Temperatures have run hotter than normal for this time of year, and no measurable rainfall has been reported since mid-fall.

- Trading volume picked up modestly, especially during Tuesday’s sell-off. Total open interest rose by 8,010 contracts to 300,315. Additionally, 1,575 bales were decertified, bringing certificated stocks down to 12,396 bales.

Supply and Demand Overview

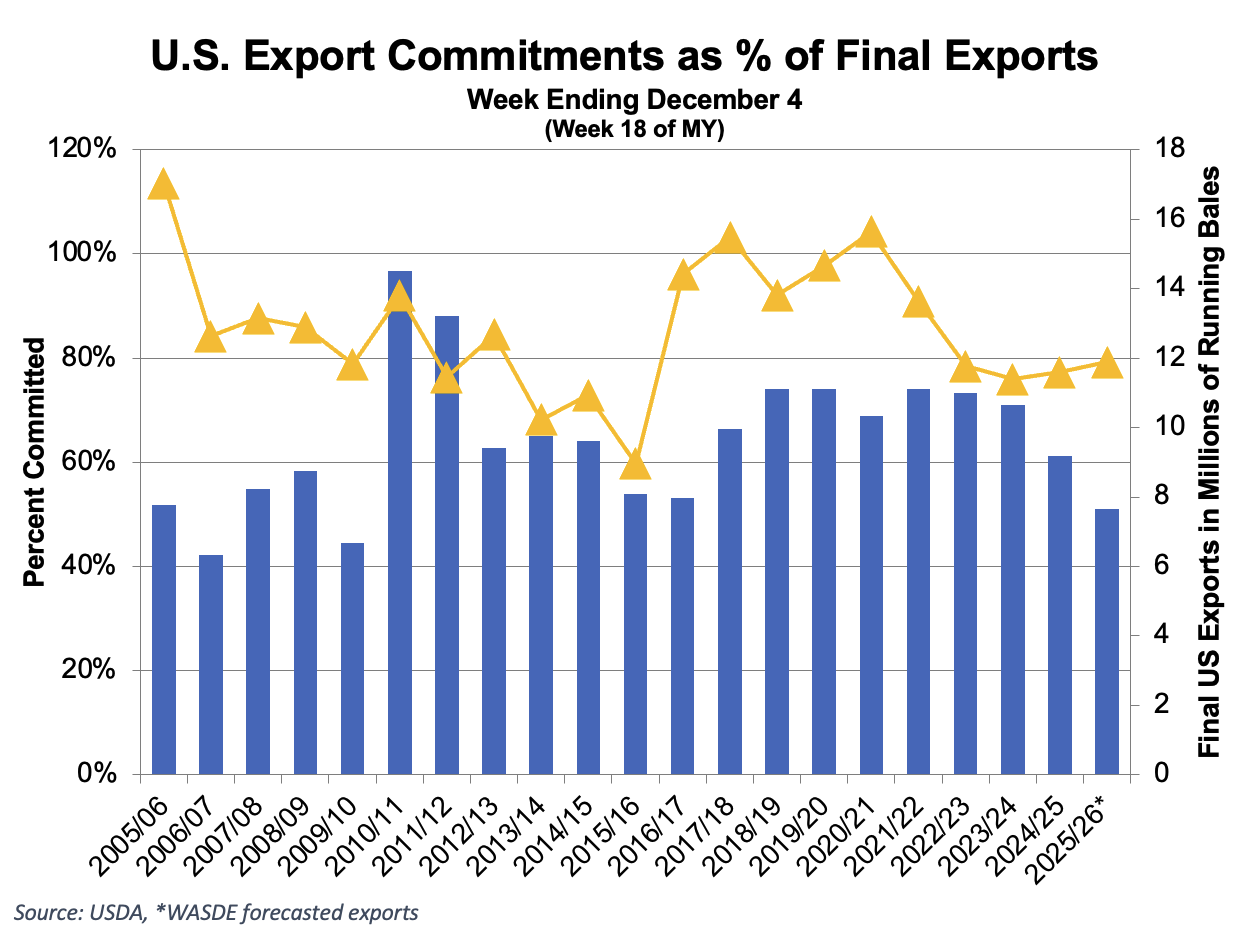

- For the week ending November 27, net Upland sales totaled 135,900 bales, with shipments of 122,100 bales, led by buying from Vietnam, Turkey, and Pakistan. Pima bookings reached 4,200 bales, while shipments totaled 7,400 bales.

- In the following week, ending December 4, net Upland sales improved to 153,200 bales, though shipments slowed to 101,600 bales. Vietnam, Pakistan, and China were the primary buyers. Pima net sales came in at 6,200 bales, with shipments at 7,600 bales. While sales improved marginally from the prior week, overall demand remains subdued, leaving total commitments behind the pace needed to reach USDA’s export projection of 12.2 million bales. One more Export Sales Report will be released before Christmas, tomorrow, December 23 at 7:30 a.m. CST. USDA continues to work through data delays tied to the government shutdown and is expected to be fully caught up by the January 8 report.

Economic and Policy Outlook

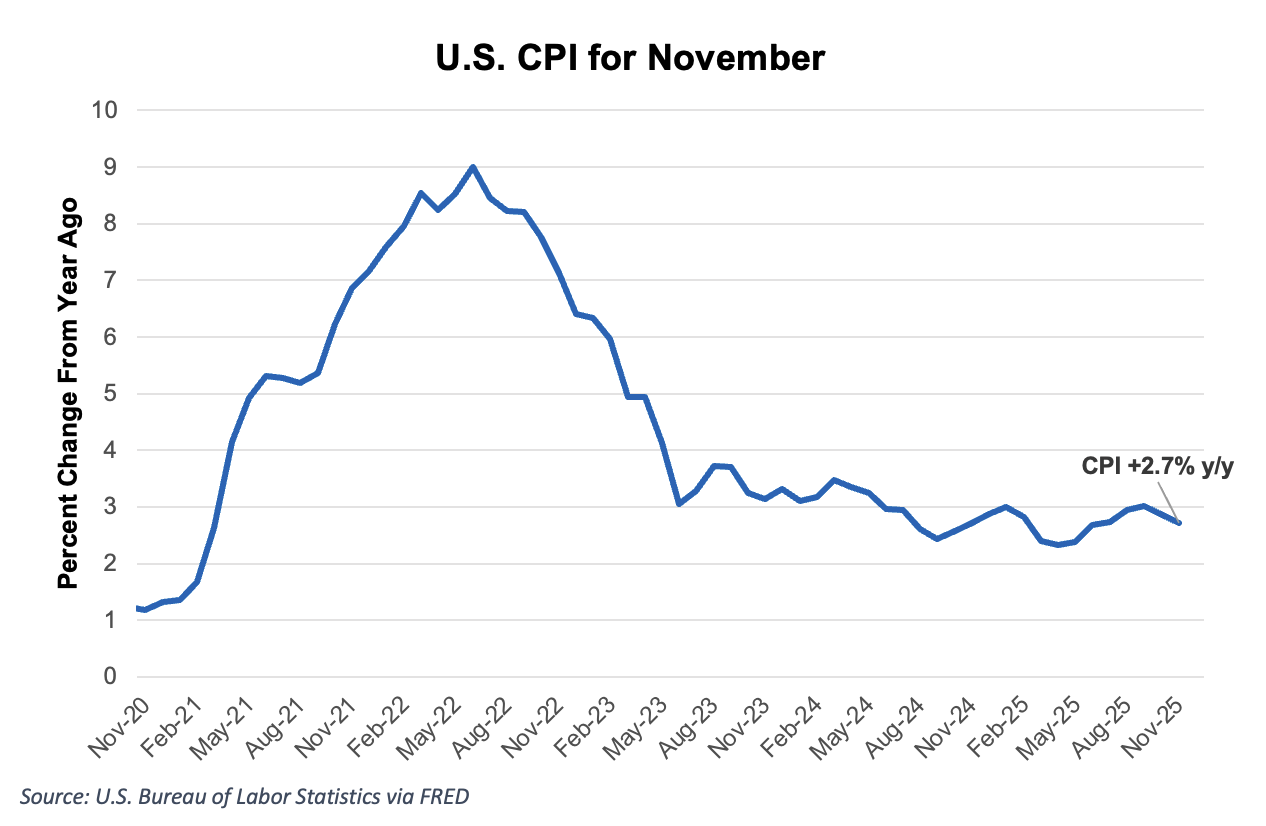

- November inflation cooled more than expected, with CPI at 2.7% and core at 2.6%, though data gaps from the government shutdown make the report difficult to fully trust. Macro pressure increased as the U.S. unemployment rate climbed to a four-year high of 4.6%, raising concerns about broader economic health. Retail sales were flat in November at 0.0% month-over-month, versus expectations for a 0.1% gain. However, select categories showed resilience, with clothing and clothing accessories up 0.9% month-over-month and 5.7% year-over-year, and furniture and home furnishings rising 2.3% month-over-month and 0.5% year-over-year. Taken together, the data point to softer growth and uneven demand, with markets now pricing roughly a 20% chance of a January rate cut and potentially two cuts in 2026.

- As mentioned last week, President Trump announced the Farmer Bridge Assistance Program, a $12 billion aid package for the 2025 crop year. Of that, $11 billion is directed toward row crops to provide near-term relief amid ongoing cost pressure and trade-related headwinds. While the program offers some support, many producers note it falls short given several years of tight margins, especially with a lower $155,000 payment cap compared to recent programs. At the same time, frustration is building around USDA’s implementation of SDRP Stage 2, where growers and insurers argue agency guidance has narrowed eligibility and altered loss calculations in ways that stray from congressional intent. Together, the two programs highlight ongoing uncertainty around disaster aid and broader financial support as producers look ahead to the 2026 crop year. There is chatter from members of Congress that it will have to step in with additional relief in the spring. House Ag Committee Chairman GT Thompson told Politico that he believes it will take another $10 billion in assistance, but there is no clear timeline.

The Seam

- As of Friday afternoon, grower offers totaled 143,394 bales. The past week, 53,412 bales traded on the G2B platform received an average price of 59.62 cents per pound. The average loan redemption rate (LRR) was 52.89, bringing the average premium over the LRR to 6.73 cents per pound.

- Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).