PCCA Cotton Market Weekly

December 29, 2025

The Week Ahead

- The Santa rally has held so far this week, with improving markets helping breathe some life back into the ag complex. Energy markets also moved higher, as oil prices were supported by cautious optimism around progress on a potential Russia–Ukraine agreement, even as ongoing geopolitical tensions surrounding Iran continue to keep markets sensitive to headlines. It should be a relatively quiet week on the data front, but optimism around the economy – following last week’s stronger GDP report – along with renewed hopes for rate cuts in 2026, has helped lift overall sentiment. Although it is a slower week, key releases to watch include the December Fed Meeting Minutes on Tuesday, the Export Sales Report on Wednesday, and the Cotton On-Call report on Friday.

- Markets will be closed Thursday, January 1, in observance of the New Year’s holiday. The cotton market will also be closed Thursday and will resume normal trading hours on Friday.

Market Recap

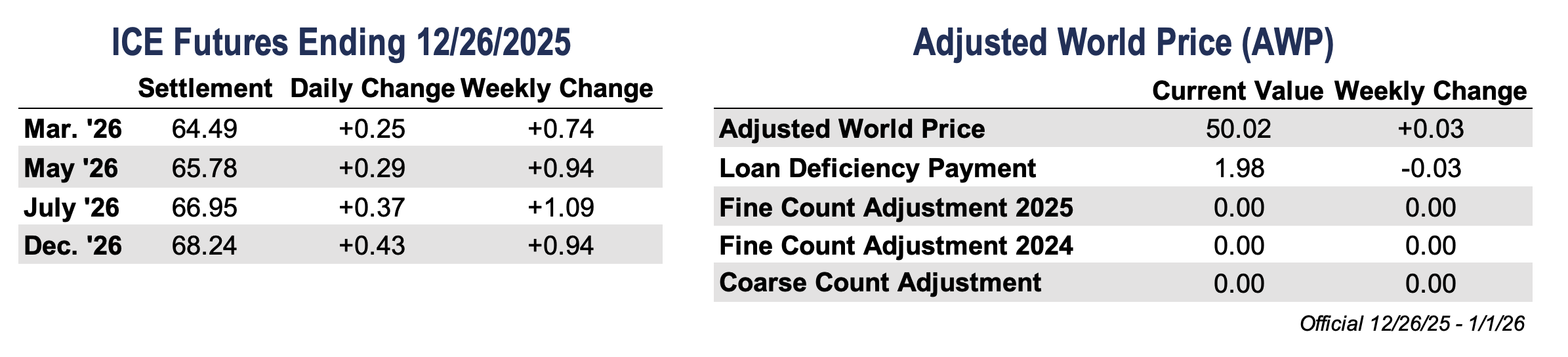

- March futures posted gains last week, reaching their highest level in more than a month. The market advanced in three of the four trading sessions, with modest but steady strength throughout the week. March futures settled Friday 74 points higher at 64.49 cents per pound, with most of the gains building ahead of the Friday close.

- Cotton prices were supported by a strong Export Sales Report and a more constructive macro backdrop. While trading was relatively quiet due to the holiday-shortened week and government closures around Christmas, volume came in slightly higher than typically expected, and the rally encouraged additional grower selling. Although technical indicators still lean bearish overall, recent price action made meaningful progress, breaking through several key resistance levels. Commitments of Traders reports are now largely caught up, with the first fully normal reporting week scheduled for release on January 9.

- Classing activity slowed briefly over the Christmas holiday, though most offices resumed operations over the weekend. As the season progresses, classing volumes continue to taper off, with a higher share of extraneous matter showing up in recent results. The Corpus Christi office did not class cotton during the holiday period and is now very near its seasonal estimate. Across the Southwest, overall classing is running just over 80% of projected totals, while West Texas remains closer to three-quarters of its expected volume.

- Trading volume picked up modestly, considering it was a holiday-shortened week. Total open interest saw a marginal increase of 222 contracts to 300,537. Additionally, 796 bales were decertified, bringing certificated stocks down to 11,600 bales.

Supply and Demand Overview

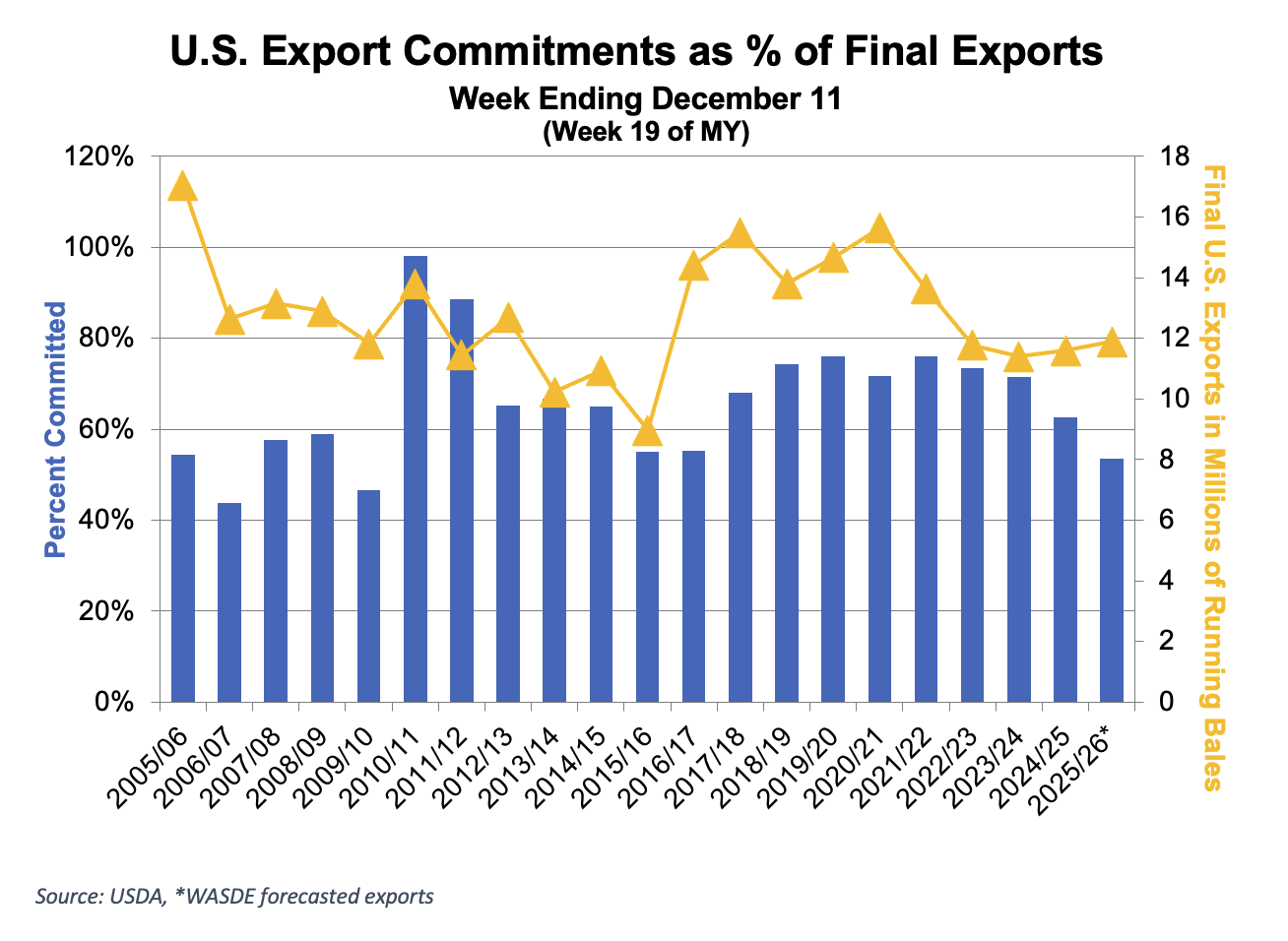

- For the week ending December 11, net Upland sales jumped to 304,700 bales, though shipments remained relatively slow at 134,400 bales. Vietnam, China, and Malaysia were the primary buyers, with China appearing on the report for a second consecutive week. That combination of strong sales and renewed Chinese interest helped give the market some traction.

- Pima net sales totaled 8,900 bales, with shipments at 3,600 bales. While overall sales improved sharply from the prior week, demand continues to be soft, leaving total commitments running behind the pace needed to meet USDA’s export projection of 12.2 million bales. The next Export Sales Report will be released Wednesday, December 31, at 7:30 a.m. CST. USDA continues to work through data delays related to the government shutdown and is expected to be fully caught up by the January 8 report.

Economic and Policy Outlook

- Fresh GDP data – released late due to the government shutdown – show the U.S. economy picked up steam in the third quarter, growing at a 4.3% annualized pace, the fastest in two years. The strength came mainly from resilient consumer spending and a boost from net exports, as U.S. goods moved more competitively into global markets. While earlier tariff-related import front-loading weighed on first-quarter growth, the economy has since settled into an average growth pace near 2.5%, broadly in line with last year. For the cotton market, a firmer economic backdrop helps support apparel demand at the margin and reinforces export competitiveness, particularly if consumer spending holds and trade flows remain active heading into 2026.

The Seam

- As of Friday afternoon, grower offers totaled 137,171 bales. The past week 46,898 bales traded on the G2B platform received an average price of 59.85 cents per pound. The average loan redemption rate (LRR) was 52.68, bringing the average premium over the LRR to 7.17 cents per pound.