PCCA Cotton Market Weekly

January 19, 2026

The Week Ahead

- The macro picture is mixed this week, despite the shortened trading schedule. Markets are closed today, Monday, January 19, in observance of the MLK holiday. Over the weekend, tariffs and the threat of additional tariffs resurfaced. Late last week, President Trump warned that countries trading with Iran could face a 25% tariff on goods. A trade deal with Taiwan was reported that would lower tariffs on goods from the country to 15%, but renewed tensions emerged over the weekend after President Trump threatened a 10% tariff on eight European Union countries backing Danish sovereignty over Greenland.

- The data calendar is lighter following last week’s heavy slate of releases, leaving markets focused mainly on tariff developments and the Fed meeting next Tuesday and Wednesday. Personal income data will be released on Thursday, but it is unlikely to draw much attention unless the number is a major surprise.

Market Recap

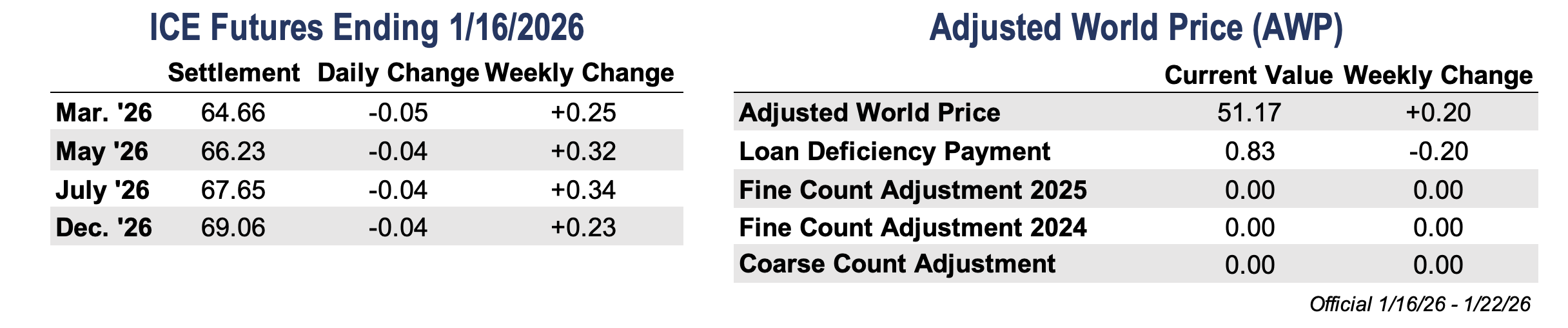

- March futures held above the 50-day moving average, though the broader technical picture remains largely unchanged. Despite last week’s supply and demand update, March futures finished only slightly higher, settling at 64.66 cents per pound, up 25 points on the week.

- Although prices finished higher on the week, cotton struggled to hold onto daily gains, with trading ranges among the narrowest seen all year. USDA supply and demand report (WASDE) released last Monday was largely absorbed without much reaction. Index fund rolling activity was underwhelming, though overall trade activity remained steady throughout the week. Tariff-related headlines continued to weigh on demand, even as November retail sales data came in strong. The imbalance in the on-call data persists but has eased slightly in recent reports. There is a chance of moisture this coming weekend across parts of the Southwest, which is badly needed. The region has seen little to no meaningful precipitation since the fall, and drought conditions have become more evident in recent months. Overall, any price strength was quickly met with selling, and broader macro headwinds offered little support.

- Daily volume was steady last week, while open interest continued to climb. Total open interest reached record levels, increasing by 16,009 contracts to 336,693, while certificated stocks were down 481 bales to 11,029 bales.

Economic and Policy Outlook

- Tariffs moved back to center stage this week, shaping much of the discussion around global trade and market sentiment. The U.S. and Taiwan reached a trade agreement that would lower tariffs on Taiwanese goods to 15% and include a sizable increase in investment by Taiwanese semiconductor firms in U.S. operations. The deal brings Taiwan’s tariff treatment in line with other major Asian trading partners and was viewed as a stabilizing development.

- At the same time, tariff threats resurfaced on multiple fronts, including potential duties tied to trade with Iran and renewed warnings directed at parts of Europe, adding to uncertainty for global markets. While these threats have grabbed attention, their effectiveness remains unclear, particularly given questions around legal authority. The Supreme Court is expected to rule soon on cases challenging the use of emergency powers to impose broad tariffs, which could limit future actions. Overall, recent developments highlight how trade policy uncertainty continues to weigh on markets, even as selective agreements move forward.

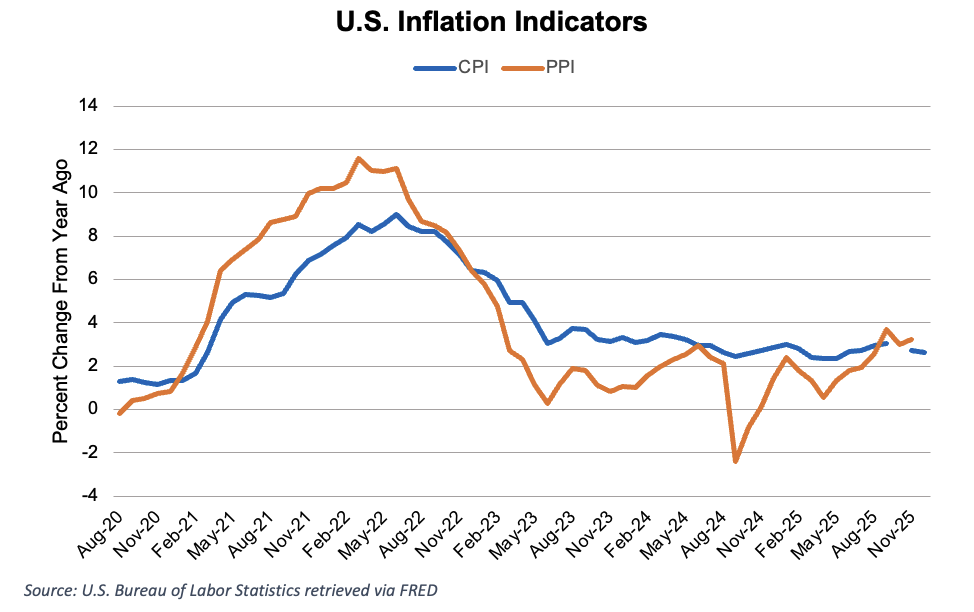

- Last week brought a heavy slate of inflation data, beginning with the December Consumer Price Index (CPI). Headline CPI rose 0.3% month over month, while core CPI increased 0.2%. On a year-over-year basis, headline CPI was up 2.7% and core CPI rose 2.6%. While the annual figures were in line with expectations, the monthly readings came in slightly below analyst estimates, offering additional evidence that inflation pressures may be easing. This data could factor into next week’s Fed meeting, though some market participants remain cautious due to data disruptions caused by the government shutdown and the absence of an October reading.

- Producer prices were more mixed, with the Producer Price Index (PPI) rising 0.2% in November and 3.0% year over year. The monthly increase met expectations, but the annual figure came in stronger than anticipated. Retail sales data for November also surprised to the upside, rising 0.6% during what is typically a strong consumer spending period. Clothing sales increased 0.9% on the month and 7.5% from a year earlier, though questions remain around how much of that growth reflects higher prices rather than increased volumes, particularly following a record-setting Black Friday.

Supply and Demand Overview

Supply and Demand Overview

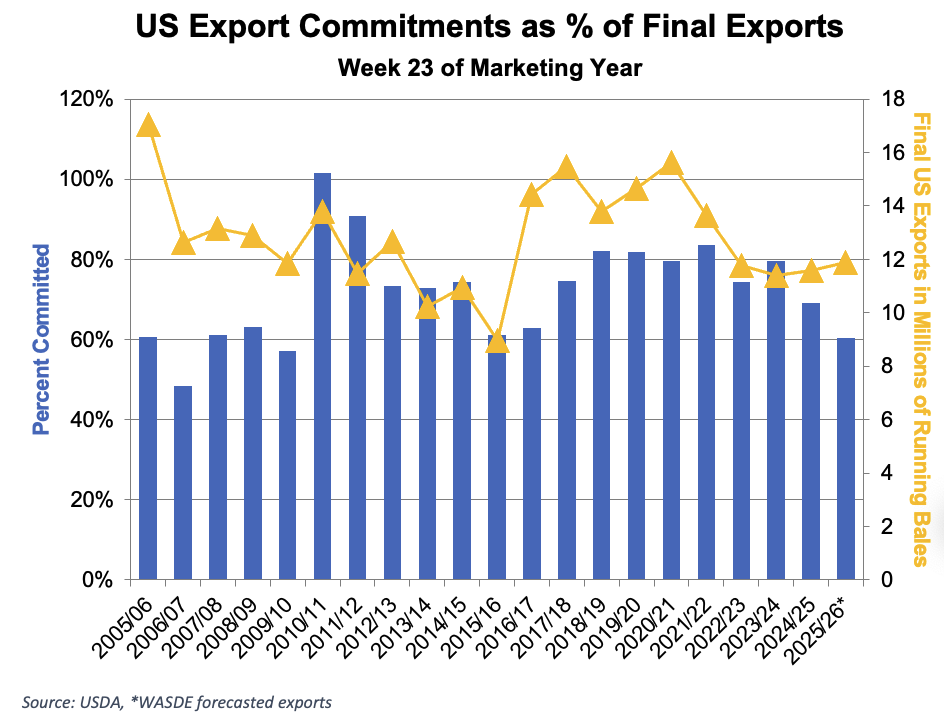

- The Export Sales Report for the week ending January 8 showed record net sales for both Upland and Pima cotton. Net Upland sales totaled 339,700 bales, while Pima sales came in at 15,700 bales. Upland shipments were below the pace needed, while Pima shipments remained strong. During the week, 156,100 bales of Upland cotton were shipped, compared with 9,800 bales of Pima.

- Even with the strong sales week, the pace still needs to pick up to reach USDA’s 12.2 million bale export projection. U.S. export sales would need to average roughly 200,000 bales per week, with shipments closer to 300,000 bales per week.

The Seam®

- As of Friday afternoon, grower offers totaled 114,525 bales. The past week, 58,850 bales traded on the G2B platform received an average price of 59.22 cents per pound. The average loan redemption rate (LRR) was 51.51, bringing the average premium over the LRR to 7.71 cents per pound.

- Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).

Sustainability Enrollment Windows

- Enrollment for the U.S. Cotton Trust Protocol will be open January 5th- April 30th, 2026. Growers who are currently enrolled will need to renew their membership to continue their involvement in the program. If your gin would like to host an Enrollment Field Day during this time, please reach out to PCCA at (806)763-8011.

- New Grower Enrollment for the Better Cotton Initiative will be open March 3rd-May 30th. Growers interested in joining this global sustainability program should contact PCCA (806) 763-8011.