PCCA Cotton Market Weekly

June 8, 2026

The Week Ahead

After a difficult start to June, the market’s focus is beginning to shift from macro-driven selling toward the supply-side story, with Thursday’s WASDE report and the June 30 Acreage report now in view.

- On the macro front, Wednesday’s CPI report will be closely watched as markets look for further clues on the timing of future Fed rate cuts. A stronger-than-expected inflation reading could support the U.S. dollar and weigh on commodity prices.

- Thursday’s WASDE report will be the primary focus this week. While major changes are not typically expected in the June report, traders will be watching closely for any adjustments to U.S. and global balance sheets ahead of the more consequential Acreage report later this month.

- July options expire Friday, which could increase volatility as the market continues its transition toward the December contract.

- The June 30 Acreage report is now less than a month away and will increasingly become a focal point for the market, particularly as traders assess whether planted acreage aligns with USDA’s March intentions.

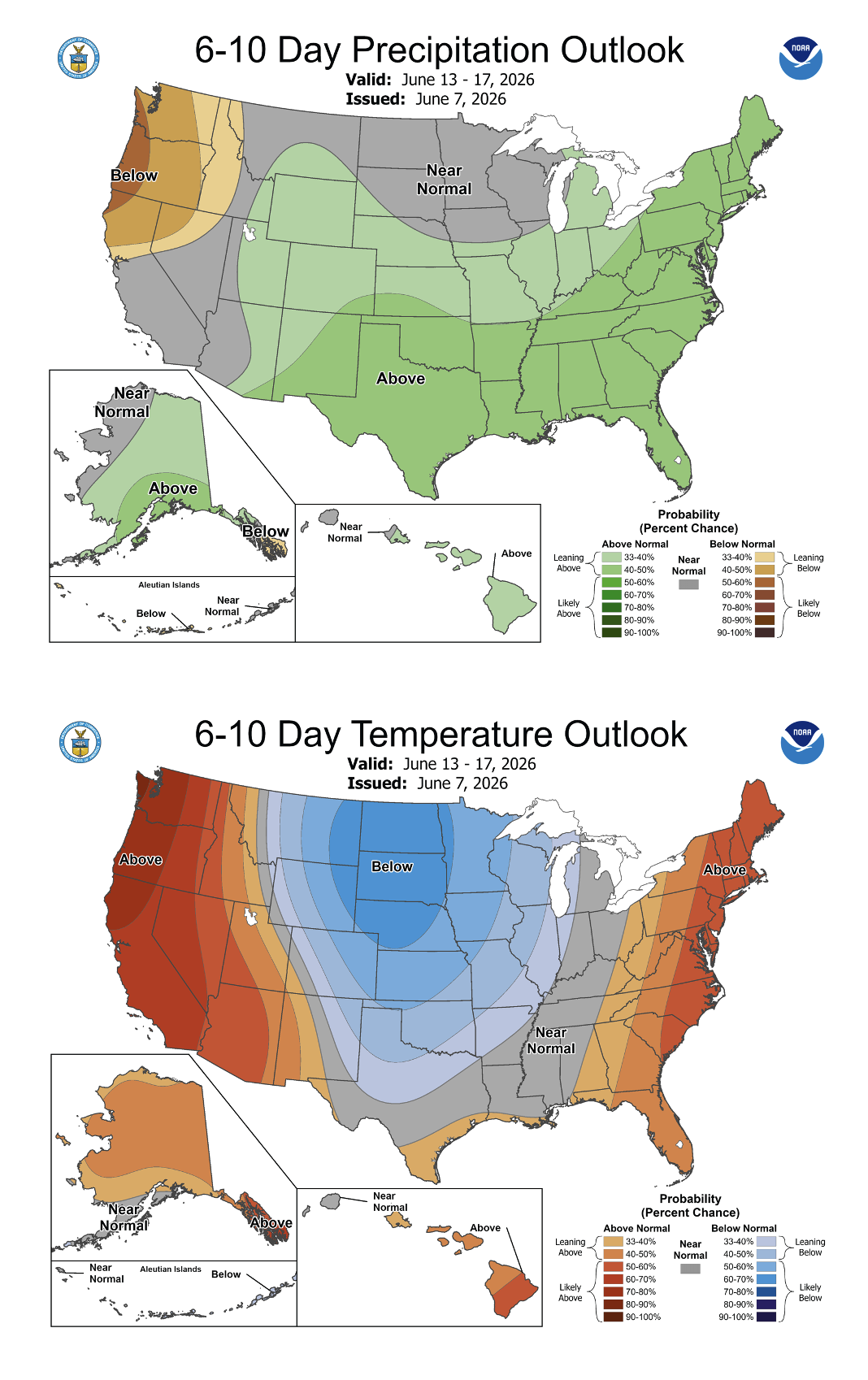

- Weather will remain closely monitored across the Cotton Belt. Recent rainfall has improved conditions in some areas, but moisture remains uneven across portions of the Southwest as the crop continues to develop.

Market Recap

- Cotton futures came under heavy pressure last week as a broad risk-off environment swept through commodity markets. Falling crude oil prices, continued fund liquidation, improving crop conditions, and a stronger U.S. dollar outweighed another week of supportive export demand and pushed futures to their lowest levels in nearly two months.

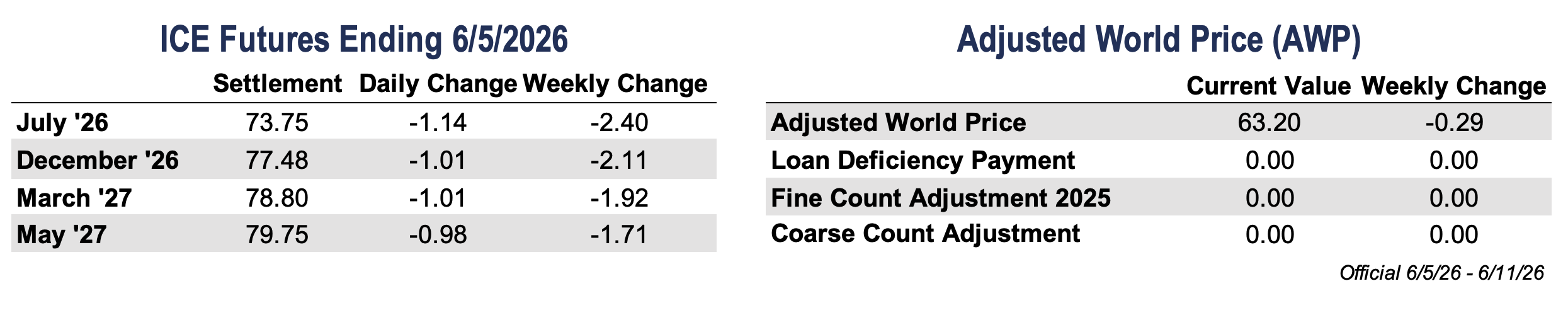

- By Friday’s close, July futures had fallen 240 points on the week to 73.75 cents per pound, while December futures lost 211 points to settle at 77.48 cents. The weakness accelerated late in the week as commodity markets sold off alongside crude oil and equity markets.

- Fund liquidation remained a major headwind. Managed Money traders were net sellers for a second consecutive week, while July open interest continued to decline as positions rolled forward ahead of First Notice Day and the start of the GSCI roll period. Open interest continued shifting toward new crop contracts throughout the week.

- Certificated stocks continued to build early in the week, climbing above 255,000 bales before easing slightly by Friday. The increase in available deliverable supply continued to pressure nearby spreads and weigh on the July contract.

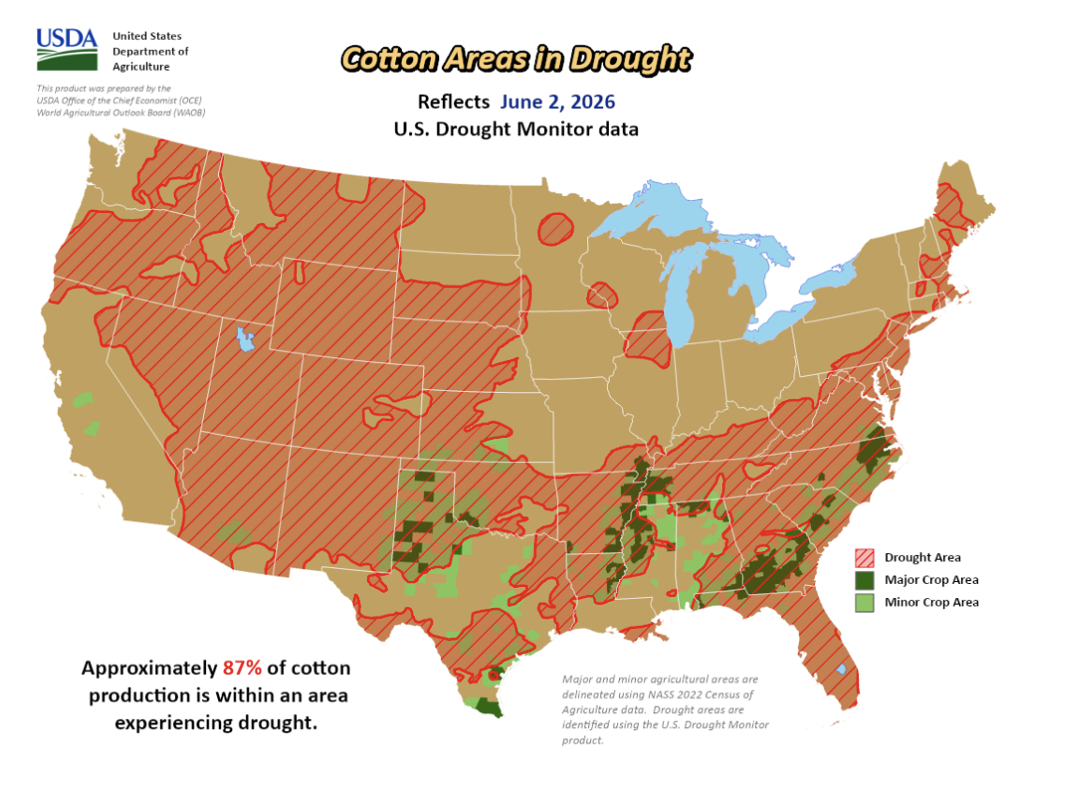

- Weather remained front and center as additional rainfall improved moisture conditions across several key production areas. USDA’s latest drought monitor showed drought coverage across U.S. cotton acreage continuing to decline, while planting progress remained near the five-year average. As a result, weather premium continued to erode from the market, particularly as forecasts called for additional moisture across portions of West Texas and other growing regions.

Economic and Policy Outlook

- Geopolitical tensions returned to the forefront over the weekend as Israel and Iran continued exchanging missile strikes, while renewed threats to shipping routes in the Red Sea added another layer of uncertainty for global trade flows. The escalation helped support crude oil prices and contributed to a cautious tone across commodity markets, though broader risk sentiment improved somewhat as investors continued to view recent weakness in technology stocks as a buying opportunity.

- Last Friday’s Nonfarm Payrolls report surprised to the upside, with the U.S. economy adding 172,000 jobs in May versus expectations of 88,000, while the unemployment rate held steady at 4.3%. The stronger labor market data pushed Treasury yields and the U.S. dollar higher as traders reduced expectations for future Fed rate cuts, creating additional headwinds for commodity markets.

- The shift in interest rate expectations sparked broad selling across financial and commodity markets, with the Nasdaq falling nearly 5%, the S&P 500 dropping 2.6%, and commodities coming under pressure as investors moved into a more defensive posture.

Supply and Demand Overview

- Overall, this week’s Export Sales Report remained supportive, with Upland sales strengthening from the previous week and shipments holding just above the pace needed to meet USDA’s current export forecast.

- For the week ending May 28, U.S. net Upland sales totaled 185,300 bales for the current marketing year, up 21% from the previous week and 62% above the prior four-week average. Vietnam led all buyers, followed by Pakistan, Turkey, China, and Bangladesh.

- New crop Upland sales totaled 77,100 bales, led by Mexico, Indonesia, and Pakistan.

- Shipments totaled 268,800 bales, down 15% from the previous week but still slightly above the roughly 267,000 bales per week needed to reach USDA’s current 12.0 million bale export projection.

- Pima activity improved, with sales totaling 5,400 bales, while shipments reached a marketing-year high of 18,700 bales. India and Vietnam led shipment activity during the week.

The Seam®

- As of Friday afternoon, grower offers totaled 907 bales. The past week 78 bales traded on the G2B platform received an average price of 70.45 cents per pound. The average loan redemption rate (LRR) was 55.55, bringing the average premium over the LRR to 14.90 cents per pound.

- Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).