PCCA Cotton Market Weekly

November 1, 2024

The cotton market moved to the lower end of its long-term trading range this week, with inquiries for U.S. cotton increasing at these lower price levels. Harvest is progressing quickly across the country, although rain in the forecast may hinder momentum. How will next week’s presidential election, November Supply and Demand Estimates (WASDE) Report, and Federal Open Market Committee Meeting (FOMC) influence the market? Get QuickTake’s read on the week’s events in five minutes.

December futures dropped below 70 cents per pound for the first time in over a month.

- Front-month futures declined in four out of five trading sessions this week, and the December contract eventually settled 196 points lower at 69.57 cents per pound.

- As prices edged lower, inquiries for U.S. cotton rose. The first of the major indexes began rolling positions from December to March, with others set to follow next week, contributing to downward pressure on the market. While technical signals were mixed, they ultimately began to point toward the downside.

- Daily volume traded was modest much of the week but picked up towards the end. Contracts were steadily added to open interest, boosting the total number of open contracts by 7,255 to 266,161, the highest level since April.

Stock markets lost momentum this week following a mix of economic news and disappointing earnings reports.

- This week saw a flurry of activity in the markets, driven by economic data, coverage of the upcoming U.S. presidential election, and third-quarter earnings reports.

- The U.S. Consumer Confidence Index rose to 108.7 in October, up from 99.2 in September, marking the most significant monthly increase since March 2021. This shift indicates that consumers' perceptions of business conditions have become more positive.

- In the third quarter, U.S. Gross Domestic Product (GDP) growth slowed to 2.8%, a slight decrease from last quarter's 3% and below the projected 3%. Consumer spending increased by 3.7% in the third quarter, which accounts for the majority of economic activity.

- The U.S. Personal Consumption Expenditure (PCE) rose by 0.2% in September and 2.1% compared to last year, aligning perfectly with expectations.

- The U.S. dollar index remained strong, while crude oil prices faced downward pressure as supply concerns eased following recent geopolitical tensions.

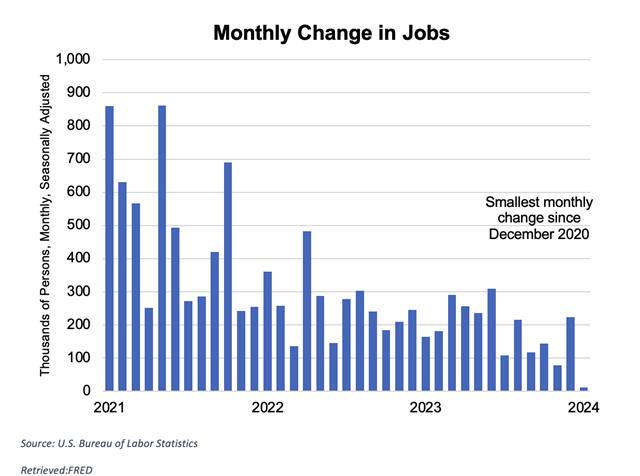

- U.S. job growth remained flat in October, with only 12,000 jobs added, while the unemployment rate held steady at 4.1%. However, recent labor strikes and hurricanes affected this figure.

U.S. export sales and shipments were average for this time of the year but have increased compared to recent weeks.

- For the 2024/25 marketing year, 189,400 Upland bales were booked.

- Inquiries into U.S. cotton have remained steady over the past week; however, mill demand still seems to be hand-to-mouth.

- Shipments of 134,300 Upland bales increased compared to the previous week but remained below the pace required to meet the current USDA export estimate of 11.5 million bales.

- Sales and shipments for U.S. Pima cotton were up for the week. Pima merchandisers sold 11,500 bales and exported 9,200 bales.

Harvest is progressing rapidly throughout the U.S. As of October 27, 52% of the crop has been harvested.

- The overall percentage of the U.S. crop rated as good to excellent declined by 4%, reaching 33%. In the Southwest, Texas saw a 6% drop, bringing its rating to 22%. Oklahoma's rating remained steady at 20%, while Kansas held steady at 43%.

- So far, 48% of the Texas crop has been harvested, 30% in Oklahoma, and 44% in Kansas.

- Harvest has continued to progress at an above-average pace across the country. The weather has been predominantly hot and dry, creating ideal conditions for harvesting. In the Southwest, clear skies have prevailed; however, a front moving in late this week and over the weekend is expected to bring rain, which could delay the harvest and affect cotton quality.

The Week Ahead

- Next week promises to be busy for the markets. With just a few days left of voting, all eyes will be on Tuesday’s presidential election, which is sure to impact trading dynamics.

- For cotton, nothing is more fundamentally important than the release of the November WASDE report, scheduled for Friday, November 8, at 11:00 a.m.

- Additionally, the Federal Open Market Committee will meet on Tuesday and Wednesday, November 6 and 7, to decide whether to maintain interest rates at the current level or implement another cut.

The Seam

As of Thursday afternoon, grower offers totaled 37,113 bales. There were 2,536 bales that traded on G2B platform with an average price of 68.11 cents per lb. The average loan was 54.19, which resulted in a premium of 13.92 cents per lb. over the loan.