PCCA Cotton Market Weekly

May 16, 2025

While the cotton market continues to react to headlines, this week brought a dose of fundamentals with the release of the 2025/26 supply and demand outlook. With uncertainty still hanging over the market, where does it go from here? Get QuickTake’s read on the week’s events in five minutes.

Cotton prices traded toward the lower end of their recent range this week.

- July futures gave up 126 points on the week, settling at 65.43 cents per pound.

- The week opened with notable developments for the cotton market, including news of a U.S.-China trade agreement and the release of the World Agricultural Supply and Demand Estimates (WASDE) report. Prices initially rose on the trade headlines but reversed course as the bearish new crop fundamentals weighed on the market. Outside of that, prices trended lower amid a weak fundamental and technical backdrop.

- Planting is underway across the Southwest, though Texas, Oklahoma, and Kansas remain slightly behind the 5-year average according to USDA’s Crop Progress Report. Recent wet conditions gave way to hot, dry weather this week, creating favorable planting conditions in some areas. However, conditions are drying quickly, and a slow rain would be welcome to support crop growth, especially in South Texas, where high temperatures and limited moisture have taken a toll.

- Trading volume was moderate this week, while open interest rose by 11,444 contracts to 228,242. Certified stocks increased to 33,100 bales with 15,963 new certifications.

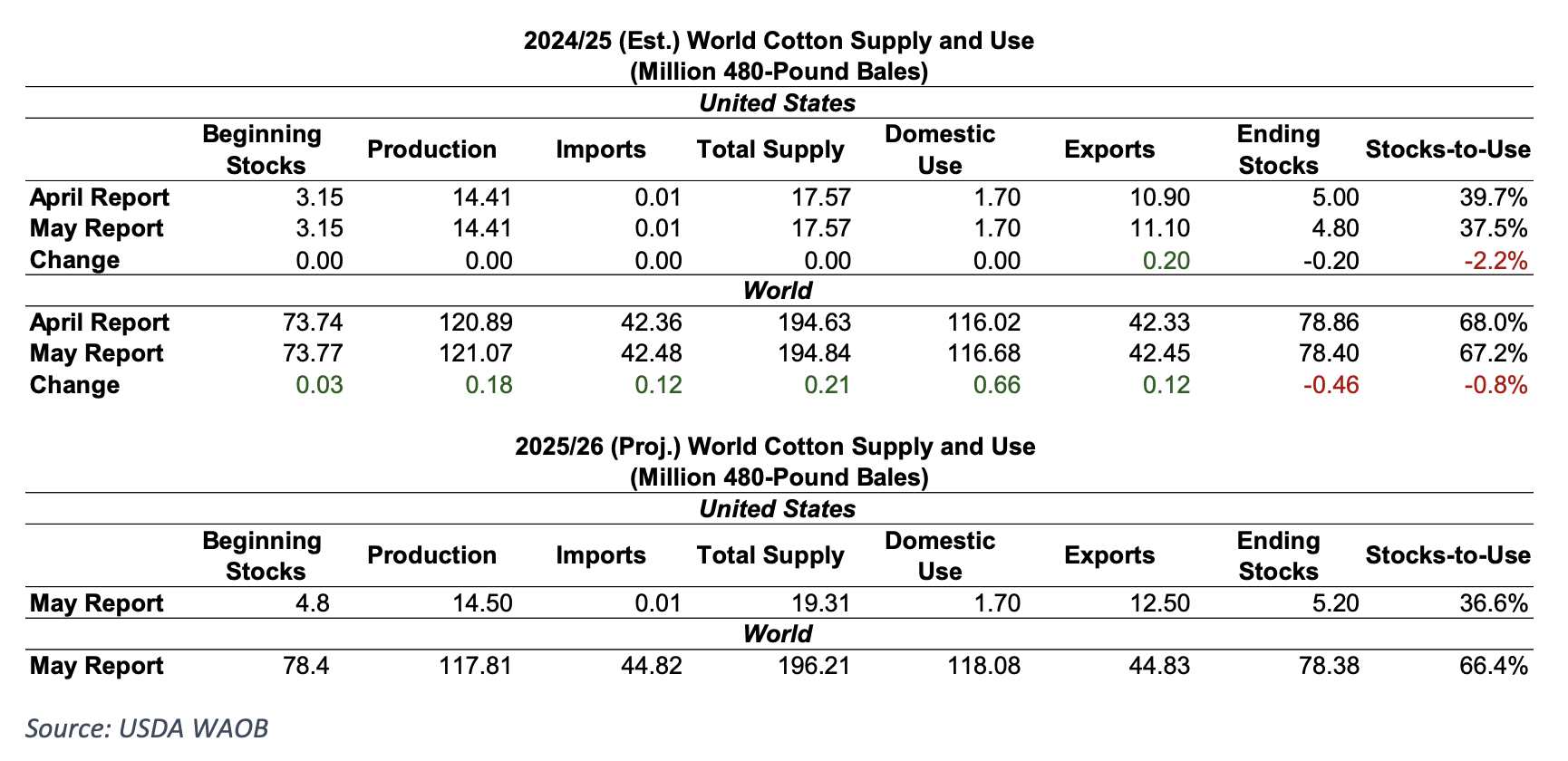

The May WASDE offered the first look at the 2025/26 crop, pointing to another potentially bearish year for U.S. cotton.

- The 2025/26 U.S. crop is projected at 14.5 million bales, with exports at 12.5 million. The production-export imbalance leaves ending stocks elevated at 5.2 million bales, resulting in a stocks-to-use ratio of 36.6%.

- The 2025/26 global balance sheet projects consumption rising to 118.08 million bales. Brazilian production and exports are expected to increase, while China’s imports remain low at a projected 7 million bales.

- The 2024/25 balance sheet saw a few adjustments. U.S. exports were raised by 200,000 bales to 11.1 million, lowering ending stocks to 4.8 million bales and the stocks-to-use ratio to 37.5%. Global consumption rose slightly to 116.68 million bales, contributing to a marginal reduction in world ending stocks. While China’s import estimate was lowered again, projections for Pakistan and Vietnam increased.

Markets reversed course and moved higher after news that the U.S. and China would roll back tariffs on each other.

- U.S. and Chinese trade officials met Saturday in Switzerland and announced a 90-day rollback of tariffs, with room for further negotiations. The U.S. will cut tariffs from 145% to 30%, while China will reduce theirs from 125% to 10%—a 115-point drop by both sides.

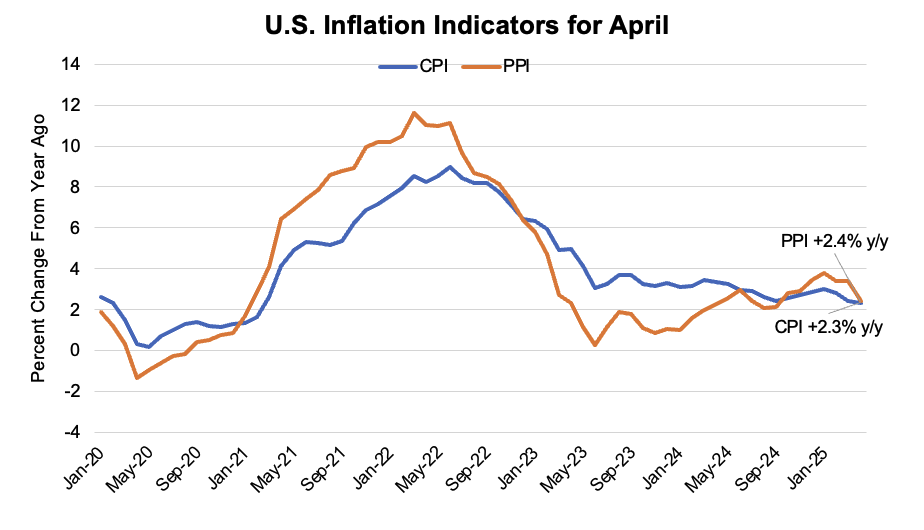

- U.S. inflation data was mixed this week. CPI came in better than expected, rising 2.3% year-over-year versus 2.4% forecast, and 0.2% month-over-month compared to 0.3% expected, suggesting cooling inflation. In contrast, PPI missed expectations, falling to a negative 0.5% on the month against a projected 0.2% decline, and rising 2.4% annually versus 2.5% expected. The decline was largely attributed to a sharp drop in final demand for services.

- U.S. retail sales slightly beat expectations, rising 0.1% month-over-month versus a flat forecast, possibly driven by consumers accelerating purchases ahead of new tariffs. Clothing and accessories sales fell 0.4% on the month but remain up 3.5% year-over-year. Furniture sales rose 0.3% from March and are up 7.8% compared to last year.

- Several parts of the reconciliation package advanced this week, with the House Energy and Commerce, Ways and Means, and Agriculture Committees approving their respective portions. These now move to the House Budget Committee, which will compile the full package from all 11 committees for markup. While the initial goal was to pass the bill before Memorial Day, that timeline now appears uncertain amid ongoing debate over whether the proposed spending cuts go too far—or not far enough.

U.S. export sales were surprisingly good while shipments remained strong for the week ending May 8.

- For the 2024/25 marketing year, U.S. merchandisers booked 122,200 Upland bales and shipped 329,200, with new crop sales totaling 34,200 bales. Sales were stronger than expected, and commitments remain above 100% of the current crop. Shipments also continue at a strong pace, possibly accelerated by tariff concerns. However, new crop sales remain sluggish, with this week’s total marking the lowest since 2016.

- Pima sales slowed from last week, with 5,000 bales booked and 9,600 shipped. Despite the dip, both remain ahead of the pace needed to meet USDA projections.

The Week Ahead

- Next week is expected to be quiet ahead of the Memorial Day holiday on Monday, May 26. Barring any headline surprises, key reports include Consumer Confidence, GDP, and Personal Income. For cotton, updates on Crop Progress and Export Sales are on deck.

The Seam

As of Thursday afternoon, grower offers totaled 42,906 bales. There were 749 bales that were traded on G2B platform during the week with an average price of 56.60 cents per pound. The average loan was 47.58, which resulted in a premium of 9.02 cents per pound over the loan.