PCCA Cotton Market Weekly

June 13, 2025

Despite fresh data and global headlines, cotton remained in its narrow range as traders weighed updated supply and demand numbers, cooling inflation, and ongoing trade tensions. Will upcoming Fed decisions and key reports be enough to shift the market’s tone? Get QuickTake’s read on the week’s events in five minutes.

The market remains rangebound, with prices ending mostly flat as broader uncertainty and seasonal pressures kept a lid on gains despite active trading.

- July futures decreased a modest 22 points during the week, settling at 65.14 cents per pound.

- As First Notice Day (FND) for the July contract approaches, the market remains in a narrow range. Trade negotiations with China caused the market to bounce higher early in the week, but the gains were short-lived. Pressure on the July contract mounted with the roll of major commodity indexes and the expiration of July options. The weight of grower on-call purchases compared to on-call sales has prompted more merchant selling as we get closer to First Notice Day for the July contract. As has been the case in recent weeks, political and economic headline risk keeps the market on edge.

- Trading volume picked up this week, though open interest fell by 5,618 contracts to 232,832. Certificated stocks climbed to 62,212 bales, driven by 8,512 new certifications, marking the highest level since June 2024. The increase in cert stocks added pressure to the market.

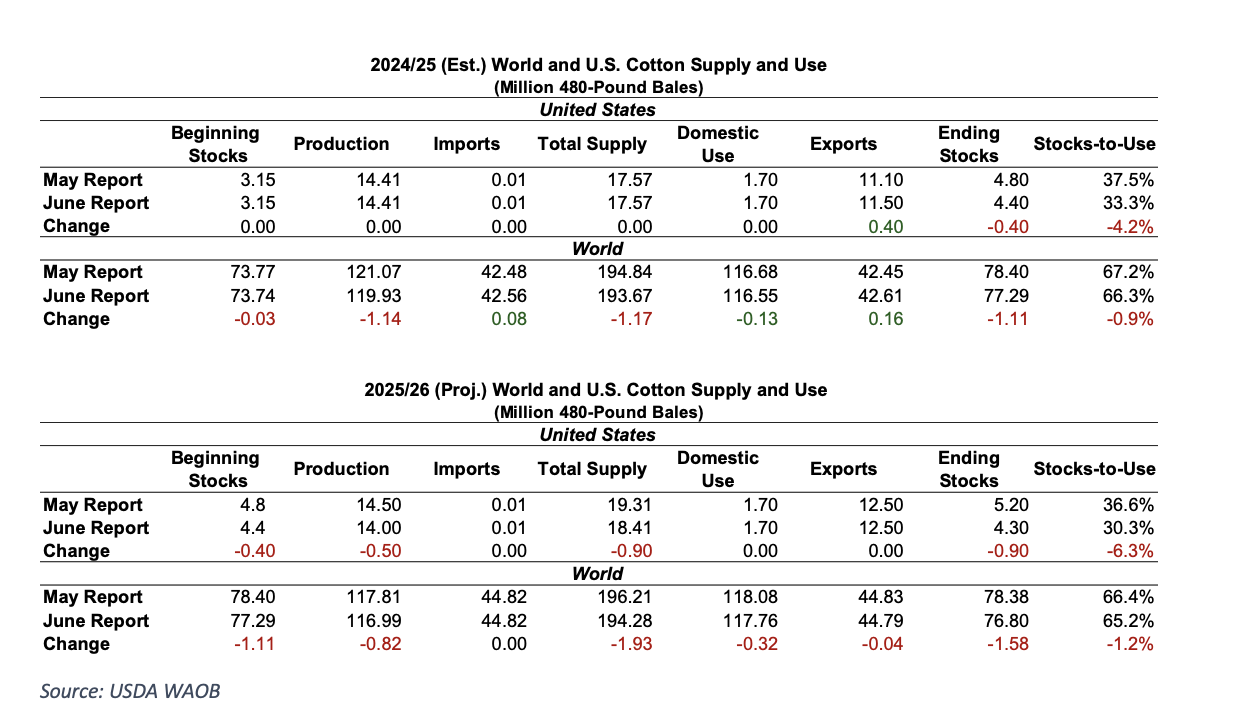

The June WASDE offered a revised outlook for 2025/26, reinforcing a tighter, but still burdensome, U.S. supply. The rare early cut to production adds a slightly bullish tilt to the new crop and marks the most market-friendly WASDE in some time.

- For the 2025/26 crop, U.S. production was lowered by 500,000 bales to 14.0 million, largely due to heavy rainfall and delayed planting in the Delta. It’s uncommon for USDA to make significant adjustments in the June report, as planted acreage is still based on March’s Prospective Plantings. A more complete picture will come with the updated Acreage Report on June 30, providing new figures for USDA to incorporate into their July estimates. Exports were unchanged at 12.5 million bales, but lower beginning stocks brought ending stocks down to 4.3 million, resulting in a stocks-to-use ratio of 30.3%.

- Globally, 2025/26 production was reduced by over 800,000 bales, with cuts in India, Pakistan, and the U.S. outweighing a 1-million-bale increase for China. Consumption was trimmed by 320,000 bales to 117.76 million while ending stocks fell by 1.58 million to 76.8 million bales. China’s import forecast remains unchanged at 7.0 million bales, while Brazil’s production and exports remain elevated.

- For 2024/25, U.S. exports were raised 400,000 bales to 11.5 million, lowering ending stocks to 4.40 million bales. Globally, consumption was adjusted slightly lower to 116.55 million, and world-ending stocks were reduced to 77.29 million bales. China’s imports stayed at 7.0 million; estimates for Pakistan and Vietnam also held steady at 5.5 and 8.0 million bales, respectively.

Markets were mostly higher this week despite lingering global uncertainty, thanks to easing inflation data and a new trade deal with China.

- The U.S. announced a new trade deal with China this week, which includes adjusted tariff rates and a mutual agreement on rare earth minerals. Under the deal, a 55% tariff will apply to Chinese exports. That consists of a 10% base tariff, 20% tied to fentanyl-related sanctions, and a 25% duty from previous trade measures. Meanwhile, goods going from the U.S. to China are set at 10%.

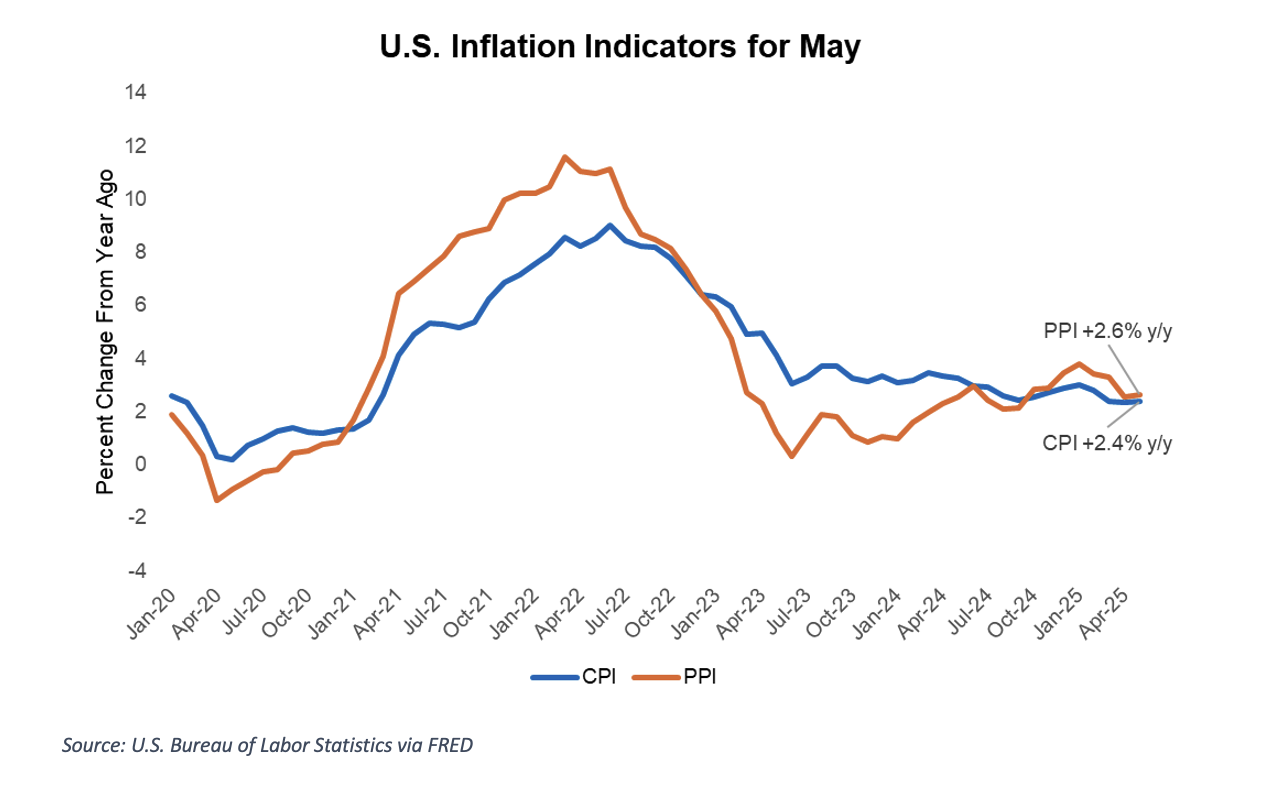

- U.S. inflation has slowed for four consecutive months, defying expectations that it would rise partly due to the ongoing trade war. The Consumer Price Index (CPI) rose 2.4% year-over-year, while core CPI, which excludes food and energy, increased 2.8%, both below forecasts. The Producer Price Index (PPI) rose 2.6% annually, which aligns with expectations, while the core PPI eased to 3.0%, coming in below estimates. Slower inflation is generally positive for commodities, easing cost pressures and supporting demand. However, with ongoing uncertainty around tariffs, markets are not in the clear yet.

- The U.S. dollar index has dropped to multi-year lows, which supports commodities by making U.S. goods more affordable for foreign buyers. At the same time, the Brazilian real, the currency of one of the U.S.’s top commodity competitors, has been strengthening.

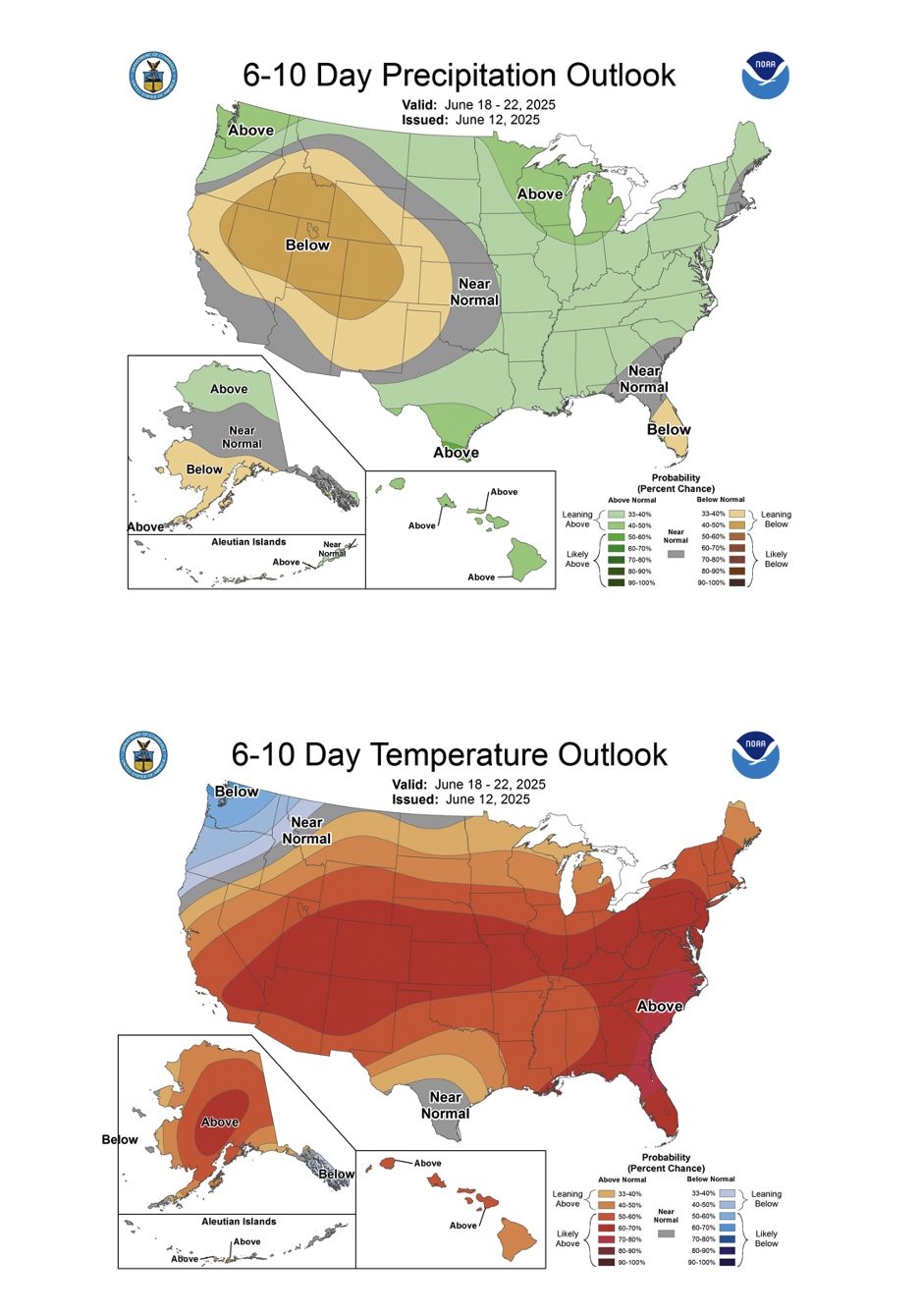

Planting across the Cotton Belt is 76% complete, just shy of the seasonal average. Progress is near normal in the Southwest—Texas is 72%, Oklahoma is 50%, and Kansas is 90% complete.

- Recent rains, cooler temperatures, and hail have raised concerns about crop damage in parts of West Texas and Oklahoma. While a drying trend should help planting progress, additional storms could impede development. In South Texas, light to moderate rain fell this week, with up to 2 inches reported in the Upper Coastal Bend. Bolls are forming in the Rio Grande Valley, but triple-digit heat adds stress. Rain chances remain elevated next week, though more consistent moisture is needed.

- Crop conditions remain mixed across the Cotton Belt, with quality hampered by excess rain and cool weather in the Mid-South and Southeast. In Texas, 37% of the crop is rated good to excellent. Kansas and Oklahoma are faring better at 67% and 50%, respectively.

U.S. cotton export sales slowed this week, with both upland bookings and shipments pulling back from recent levels.

- For the 2024/25 marketing year, U.S. merchandisers booked a net of 60,200 Upland bales and shipped 236,300. New crop sales reached 36,100 bales, and total outstanding sales for the next marketing year remain at the lowest level since 2015. Sales were down sharply, 45% from the week prior, but total commitments remain well above USDA’s 11.5 million bale target. Shipments also dipped, falling 25% week-over-week.

- Pima activity slowed further, with net sales of just 1,400 bales and shipments down to 5,800 bales. Despite the pullback, overall exports remain on pace with USDA projections.

The Week Ahead

Next week will be a shortened trade week, with markets closed Thursday, June 19, for the Juneteenth holiday. Attention will turn to the FOMC meeting on Tuesday and Wednesday, where the Fed’s tone could influence broader market sentiment. Cotton traders will have fresh data to digest, including Crop Progress, retail sales, and a delayed Export Sales Report – now set for release on Friday, June 20.

The Seam

As of Thursday afternoon, grower offers totaled 43,731 bales. There was no trading activity on the G2B platform this past week.