PCCA Cotton Market Weekly

March 30, 2026

The Week Ahead

Markets will likely remain driven by geopolitics, with Middle East developments and energy price volatility continuing to outweigh traditional fundamentals in the near term.

- Geopolitical risk and crude oil will stay in the driver’s seat, keeping markets headline-driven and sentiment reactive. While the macro calendar is relatively light, delayed retail sales on Wednesday and labor data on Friday, including unemployment and the unemployment rate, will be monitored for broader economic signals. Overall, the macro tone remains mixed, with energy markets continuing to set direction across commodities.

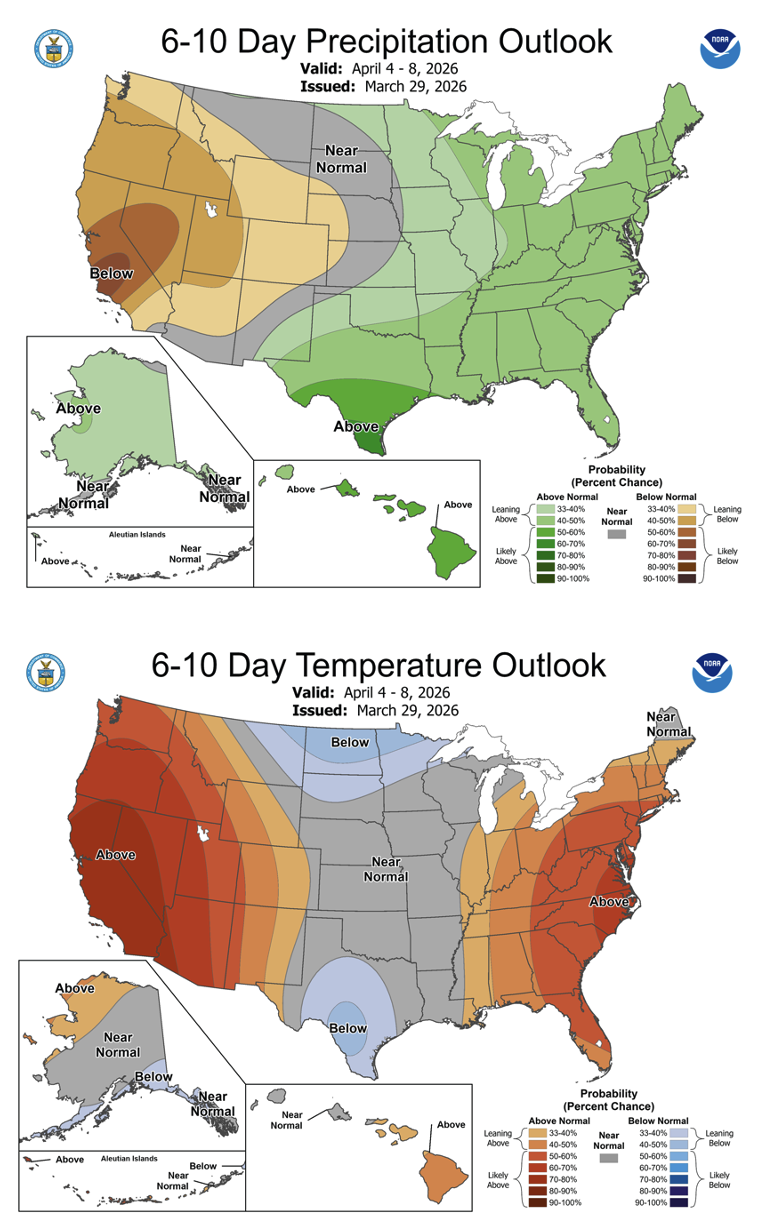

- On the ag side, attention turns solely to Tuesday’s USDA Prospective Plantings report, the next major fundamental catalyst. The report will provide an updated view of 2026/27 cotton acreage, though expectations remain uncertain given recent price volatility and persistent dryness across the cotton belt. For the 2025 crop year, 9.3 million acres were planted across the Cotton Belt. As a reminder, USDA’s Outlook Forum in February projected 9.4 million acres, while the National Cotton Council survey came in lower at 8.99 million acres. Beyond next week, focus will quickly shift to additional macro and USDA updates, but for now, markets are counting down to Tuesday as the next key driver.

Market Recap

- Cotton futures moved higher through the week, with May pushing to its highest levels in over a year before a volatile Friday session that saw prices reverse from the highs but still finish stronger on the day. May futures settled 215 points higher at 69.46 cents per pound, briefly extending the breakout above the 200-day moving average before stalling.

- Early strength was driven by fund buying, improving technicals, and support from volatile crude oil tied to the Iran conflict, but markets turned more cautious as the week progressed amid shifting headlines, inflation concerns, and uncertainty around policy signals. Late-week pressure followed after cotton expectations from the “Celebration of Agriculture” event failed to materialize, prompting a reversal from the highs. Overall, the market showed resilience despite macro uncertainty, but remains sensitive to demand, geopolitical developments, broader financial markets, and worsening drought conditions ahead of planting, with attention now turning to the upcoming USDA Prospective Plantings report.

- Continued buying in the latest Commitments of Traders report helped support market strength, while on-call activity improved for a sixth consecutive week as the imbalance narrowed. Trading activity strengthened into the end of the week, with the heaviest volume occurring on Thursday and Friday as prices moved higher. Open interest increased 14,024 contracts to 343,170, while certificated stocks decreased 975 bales to 114,665.

Economic and Policy Outlook

- The White House hosted a high-profile agriculture event where President Donald Trump signaled support for a range of farm policy measures, including biofuels, aid programs, and reinforcing the need to pass a Farm Bill. While there were rumors that BACA would be mentioned, it was not addressed, leaving some disappointment. Overall, the event underscored ongoing efforts to support farm income amid elevated input costs, policy uncertainty, and broader trade and legal pressures.

- Geopolitical developments surrounding the Iran conflict remained a central influence on markets this week, with sentiment shifting alongside evolving headlines. President Donald Trump extended the pause on attacks targeting Iranian energy infrastructure out to ten days, signaling that negotiations are ongoing, though uncertainty remains. At the same time, discussions around a potential increase of up to 10,000 additional U.S. troops in the region added to the risk backdrop. Iran has rejected a U.S. proposal to end the conflict and instead put forward its own conditions, highlighting the complexity of reaching a resolution. The continued back-and-forth has kept crude oil volatile and markets reactive, reinforcing a headline-driven environment.

- President Donald Trump announced that his meeting with Xi Jinping has been rescheduled for May 14–15 in Beijing after being pushed back due to the Iran conflict, putting U.S.–China trade back in focus. Early discussions are already underway, with agriculture expected to be a key part of the conversation, including potential purchases of U.S. commodities and renewed attention on Phase One enforcement. The news provided some support to commodity markets this past week, and looking ahead, the meeting will be an important gauge of whether recent dialogue can translate into tangible trade progress, particularly for U.S. agriculture, amid elevated broader geopolitical uncertainty.

- The Senate moved to end the DHS funding standoff by passing a measure to fund most of the agency while leaving immigration-related components to be addressed later, effectively pushing the more contentious issues down the road. However, the situation remains unresolved as House Republicans have rejected the Senate bill and are now considering an alternative approach, prolonging the stalemate. Looking ahead, uncertainty remains around how and when a resolution will be reached, with ongoing disagreements over immigration funding and broader policy priorities likely to keep this issue in focus.

Supply and Demand Overview

- U.S. export sales were slightly improved for the week ending March 19. Net upland sales totaled 202,400 bales, up 3% from the previous week but down 5% from the prior four-week average, with Vietnam, Pakistan, and Turkey leading the buying. New crop sales came in at 27,000 bales, primarily to Peru and Honduras. Pima sales were also strong at 30,900 bales, a marketing-year high, while shipments improved to 7,800 bales.

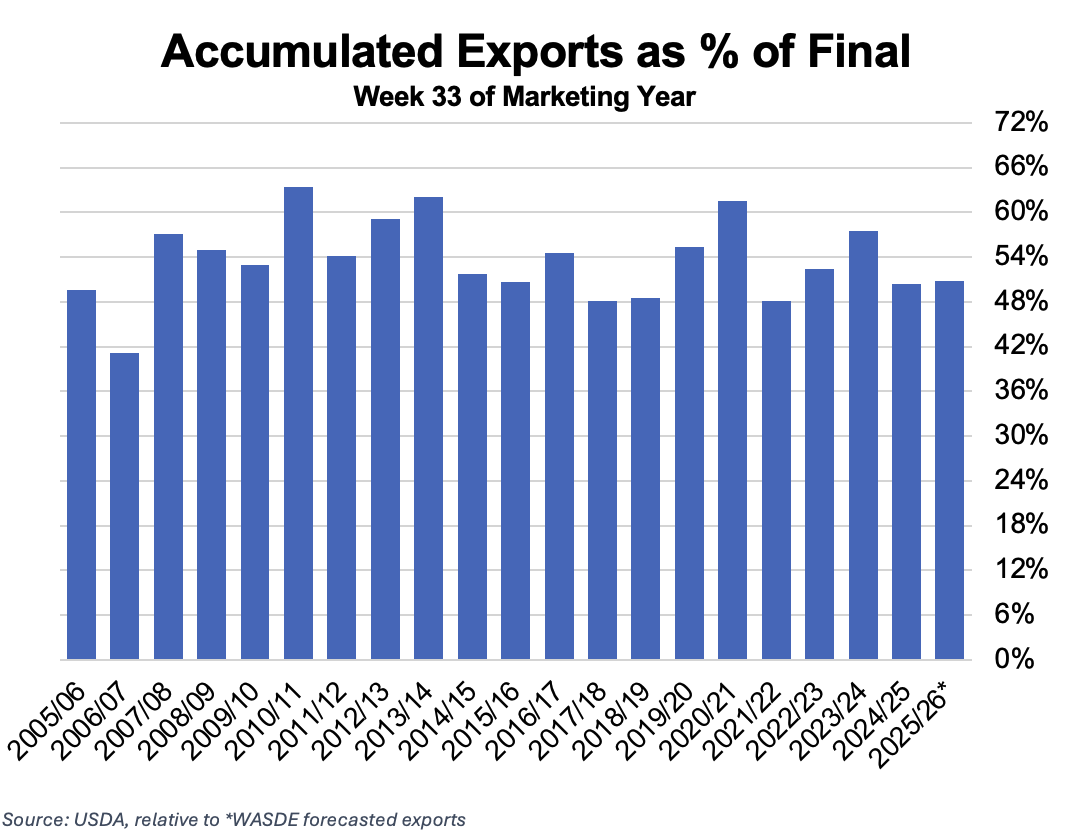

- Shipments were a standout at 400,600 bales, a marketing-year high and well above the recent pace. Moving forward, shipments will need to average just under 300,000 bales per week to reach USDA’s 12 million bale export estimate. Overall, a solid report driven by strong export movement, though there is still a long way to go. That said, we are in the peak shipping window, and this week was a step in the right direction.

The Seam®

- As of Friday afternoon, grower offers totaled 24,068 bales. The past week, 6,378 bales traded on the G2B platform received an average price of 60.70 cents per pound. The average loan redemption rate (LRR) was 50.26, bringing the average premium over the LRR to 10.44 cents per pound.

- Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).

Sustainability Enrollment Opportunities

Sustainability Enrollment Opportunities

- Enrollment for the U.S. Cotton Trust Protocol will be open January 5th- April 30th, 2026. Growers who are currently enrolled will need to renew their membership to continue their involvement in the program. If your gin would like to host an Enrollment Field Day during this time, please reach out to PCCA at (806) 763-8011. Click here for a list of in-person sign-up dates.

- New Grower Enrollment for the Better Cotton Initiative will be open from March 3 to May 30. Growers interested in joining this global sustainability program should contact PCCA (806) 763-8011.