Cotton Prices Continue Range Bound

By Dr. Don Shurley

Jul 24, 2025

Cotton prices (December futures) continue in the mostly 67-to-71 cents range. Thus far, nothing has been able to push prices higher for the past seven months. We’ve had a few dips below this range, but prices recovered quickly.

For the producer looking for 2025 crop opportunities in the 70s (and who isn’t), it’s been an agonizing and disappointing journey so far. Few growers will contract in the 60s and instead will choose to wait and hope for something better. Some, however, may have taken protection with Puts.

USDA’s July production and supply/demand numbers are pretty much a non-factor. There are a few changes worth noting and keeping track of, but nothing of major consequence:

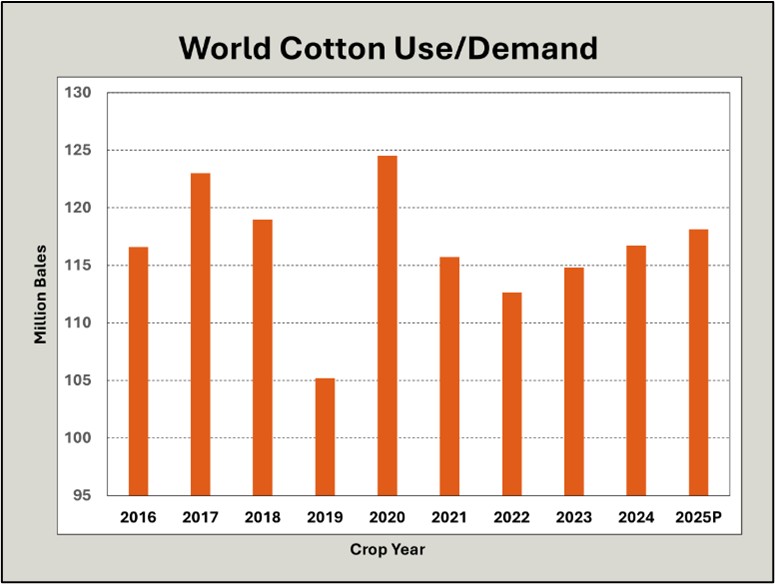

After the big COVID pandemic decline in 2019, Use rebounded strongly in 2020 but then declined in 2021 and 2022. Since then, Use has now increased three consecutive years (2025 projected) — averaging a 1.6% increase per year.

While this is good, it has yet to translate into stronger prices for U.S. growers. This is likely due, at least in large part, to (1) market uncertainties during the year and (2) loss of World export market share, primarily to Brazil. I would not consider cotton’s market demand to be “back” or “resurgent” until World Use is at 120 million bales or better. Use is projected at 118.12 million bales for the 2025 crop marketing year.

So, what’s ahead? I’m trying to look for anything that could possibly give us an increase in price:

As of July 20, the U.S. crop is 13% poor and very poor and 57% good to excellent. This shows improvement over recent weeks. Texas is 18% poor and very poor, down from 25% earlier. Tennessee is 25% poor or very poor.